Weekly Market Cheat Sheet, May 22, 2017

The Sevens Report is the daily markets cheat sheet our subscribers use to keep up on markets, leading indicators, seize opportunities, avoid risks and get more assets. Get a free two-week trial with no obligation, just tell us where to send it.

Last Week in Review:

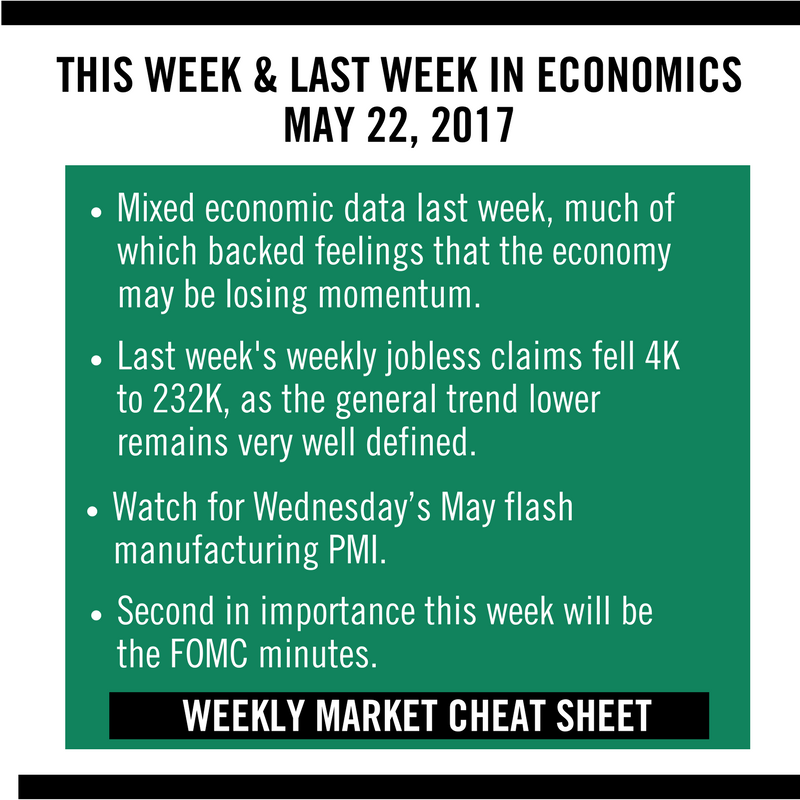

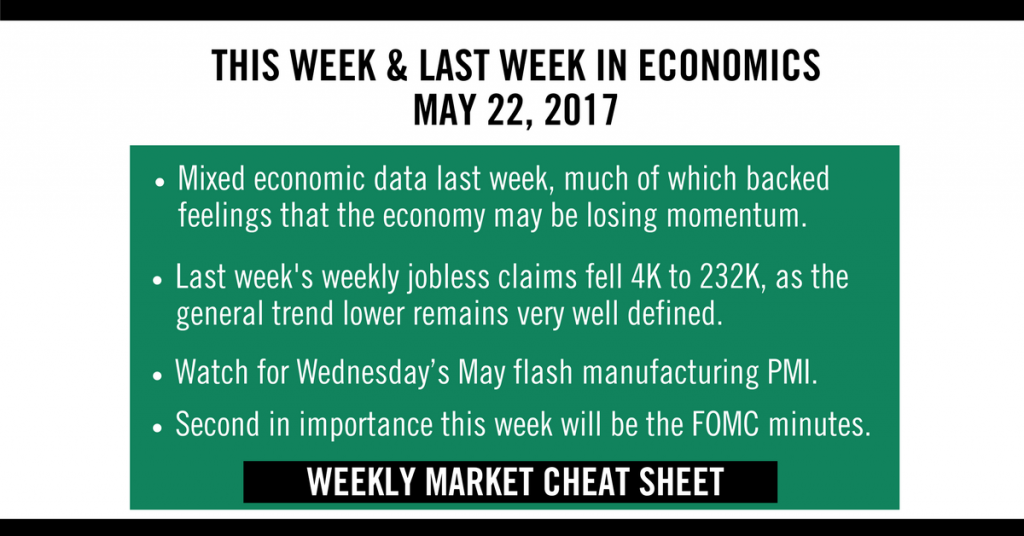

There weren’t many economic reports last week, and the data we did get was mixed. In sum the data did nothing to remove the growing feeling that the US economy is losing momentum.

First, the initial look at May data in the form of the Empire State Manufacturing Index badly missed at -1.0 vs. (E) 8.0, but the Philly Fed Business Outlook Survey on Thursday contrarily blew away expectations (38.8 vs. E: 19.6). The net effect is that it put more focus on this week’s flash manufacturing PMI to give us a true look at the pace of manufacturing activity in May.

In the US housing market, the Housing Market Index beat expectations on Monday (70 vs. E: 68), but Housing Starts data on Tuesday whiffed (1.172M vs. E: 1.256M).

The most encouraging report last week was Industrial Production, which beat estimates of 0.4% with a headline print of 1.0%. But, a lot of that “beat” came from auto manufacturing, and activity in that sector has almost certainly peaked (remember Ford is cutting employees amidst more challenging sales environments). Point being, the Industrial Production beat is likely a one off, not the start of a trend.

Rounding things out with the labor market, weekly jobless claims fell 4K to 232K, as the general trend lower remains very well defined. Continuing claims fell to a 29-year low while its four-week moving average fell to a 43-year low. This encouraging report was especially notable because the data was collected from the week corresponding with the survey week for the May jobs report, and the strong print suggests that May could be another very strong month for the labor market. Bottom line, economic data last week did not materially change our outlook for the markets.

This Week’s Preview:

This will actually be a relatively busy week of economic data, as we get the flash manufacturing PMIs, Fed minutes from the May meeting, and other important economic reports.

The most important report this week will be Wednesday’s May flash manufacturing PMI. This will be the first major data point for May and it needs to show stabilization and, better yet, acceleration for stocks to rally.

Second in importance this week will be the FOMC minutes. Markets have priced in a slightly more dovish Fed given the soft inflation data recently, but markets have overestimated the Fed’s dovishness throughout 2017. If the minutes are hawkish, that could push yields and the dollar higher (which would be stock positive).

Meanwhile, there are two reports on housing data, New Home Sales and Existing Home Sales due out on Tuesday and Wednesday, respectively. Investors would welcome a rebound after last week’s soft Housing Starts report.

Finally, both the second look at Q1 GDP and Durable Goods Orders will be released Friday morning. The latter will be closely watched as the gap between soft and hard data remains a concern, and a strong revision to GDP and a good Durable Goods number will help close that gap. Bottom line, economic data remains the key to reigniting the reflation trade (remember, it’s #1 in my list of four events needed to restart the rally). So, the market needs good data and a confident/hawkish Fed for stocks to again test recent highs.

Get the simple talking points you need to strengthen your client relationships with the Sevens Report. Everything you need to know about the markets delivered to your inbox by 7am each morning, in 7 minutes or less.

")

")