Understanding What’s Happening in the UK and with the BOE (This Matters to U.S. Stocks and Bonds)

What’s in Today’s Report:

- Understanding What’s Happening in the UK and with the BOE (This Matters to U.S. Stocks and Bonds)

- What the Nordstream Pipeline Sabotage Means for Energy Markets

Futures are down close to 1% on digestion of Monday’s bounce and as UK PM Truss defended her spending plan.

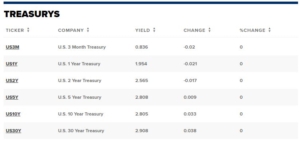

UK Prime Minister Truss doubled down on her tax cut and spending package, calling it the “right plan.” The market still disagrees, however, and the Pound is down –0.5% and 10-year GILT yields are up 14 bps on the comments.

Economically the only notable report was EU Economic Sentiment which missed estimates (93.7 vs. (E) 96.0).

Today the key economic report will be weekly Jobless Claims (E: 218K) and as we’ve consistently said, the sooner this number moves towards 300k, the better for markets. We also get the final Q2 GDP (E: -0.6%) and there are two Fed speakers, Mester (1:00 p.m. ET) and Daly (4:45 p.m. ET) but they shouldn’t move markets.

Like the past several days, the British Pound and 10-year GILT yields will drive global markets. If the Pound drops and GILT yields rise further, stocks will fall and could give back most, if not all, of yesterday’s gains.