Tom Essaye Quoted in Benzinga on August 12, 2021

3 Things That Could Send The S&P 500 Down 20%

The consensus expectations for the Federal Reserve monthly asset purchasing is that the Fed…Essaye said. Click here to read the full article.

The consensus expectations for the Federal Reserve monthly asset purchasing is that the Fed…Essaye said. Click here to read the full article.

What’s in Today’s Report:

Stock futures are little changed this morning as investors digest Monday’s hawkish Fed chatter and continue to monitor the status of the Delta variant outbreak around the globe.

Economically, Germany’s August ZEW Survey was moderately disappointing while domestically, the NFIB Small Business Optimism Index came in at 99.7 vs. (E) 103.3, however neither report is materially moving markets given the recent focus on the very strong July jobs report in the U.S.

On infrastructure, the $1.2T bipartisan bill is expected to pass a final vote in the Senate later this morning but that has largely been priced into markets already.

Today, there is one economic report to watch: Productivity and Costs (E: 3.5%, 1.2%) and one Fed speaker: Evans (2:30 p.m. ET).

Additionally, there is a 3-Year Treasury Note auction at 1:00 p.m. ET, and a soft outcome could result in another wave of hawkish money flows like we saw on Monday (yields higher, dollar higher, mixed price action in equities).

Rising COVID cases will only hurt the market if they result in a change in…Tom Essaye, a former Merrill Lynch trader who writes the “Sevens Report” newsletter, wrote in a note. Click here to read the full article.

The July jobs report reinforces the fact that the Fed will reduce its quantitative easing over the…Tom Essaye, founder and chairman of Sevens Report Research said. Click here to read the full article.

Negatively, there remain aggressive buyers on Treasury dips and it’s going to take a real, impactful headline…Tom Essaye of Sevens Report said in a note. Click here to read the full article.

![]()

The 10-year yield bounced off the 1.13% level (which seems to be support) and clearly the 10-year can react…Tom Essaye, founder of the Sevens Report Research, said in a note. Click here to read the full article.

![]()

What’s in Today’s Report:

Futures are slightly lower following a mostly quiet weekend of news as there were no major changes to the COVID outlook or the economic recovery.

Economic data was solid as German and Chinese exports for July both beat estimates.

Chinese CPI rose 1% vs. (E) 0.8% and that may reduce the amount of stimulus officials unleash on the economy (so potentially negative for global growth).

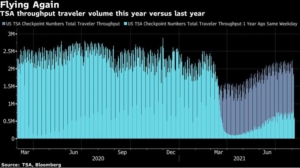

Today focus will be on JOLTS (E: 9825M) and on Fed commentary following the jobs report (Bostic at 10:10 a.m. ET and Barkin at 11:20 a.m. ET). But, unless JOLTS are a major surprise or Fed officials are shockingly hawkish, these events shouldn’t move markets. As such, the tenor of COVID headlines (and whether we are seeing behavior changes) will continue to drive markets in the near term.

What’s in Today’s Report:

Futures are little changed ahead of this morning’s jobs report.

Economic data underwhelmed overnight with Japanese Household Spending falling –3.2% while German Industrial Production missed estimates (-1.3% vs. (E) 0.5%).

On COVID, headlines remain net negative as cases continue to rise and analysts look for any signs of a loss of economic momentum (so far there’s nothing concrete).

Today the focus is on the jobs report and expectations are as follows: Job Adds: 900K, UE Rate: 5.7% and Wages: 0.3% m/m and 3.8% y/y. Again, the biggest risk to markets is for a “Too Hot” jobs number that shifts the tapering timeline, and if that occurs we should brace for volatility.

On the earnings front, most of the systemically important companies are behind…wrote Tom Essaye in a recent memo. Click here to read the full article.

Markets look ahead to key economic data in the…wrote Tom Essaye, founder of Sevens Report Research before the jobs report hit the wires. Click here to read the full article.