Last Week and This Week in Economics, May 1, 2017

The Sevens Report is everything you need to know about the markets by 7am each morning in seven minutes or less. Free trial at 7sReport.com.

Economic data continued to underwhelm last week and the gap between soft sentiment surveys and actual, hard economic data remains wide, and that gap remains a medium term risk on the markets.

Last week in Economics – 4.24.17

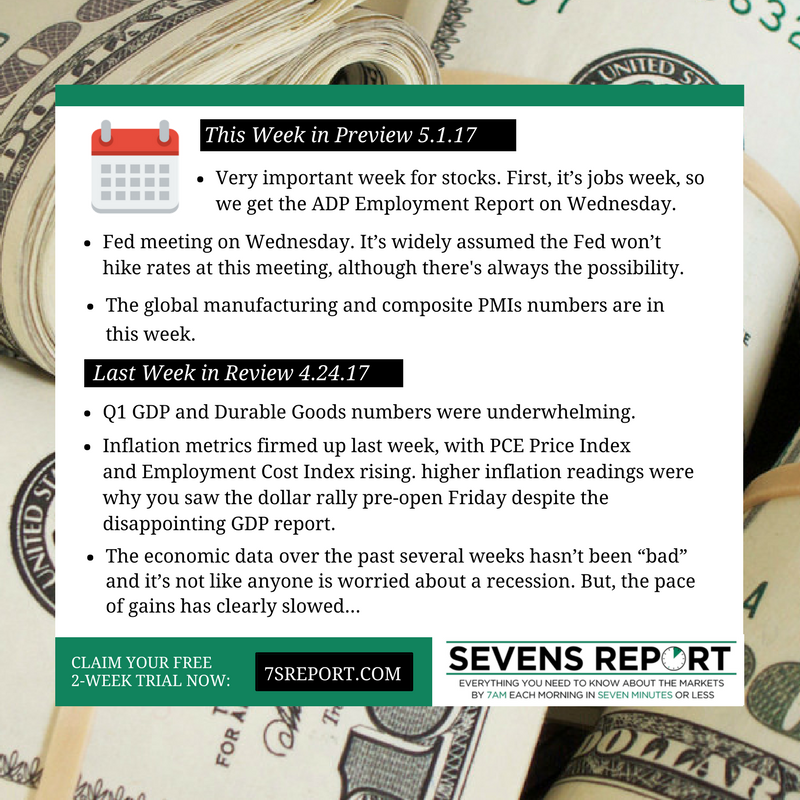

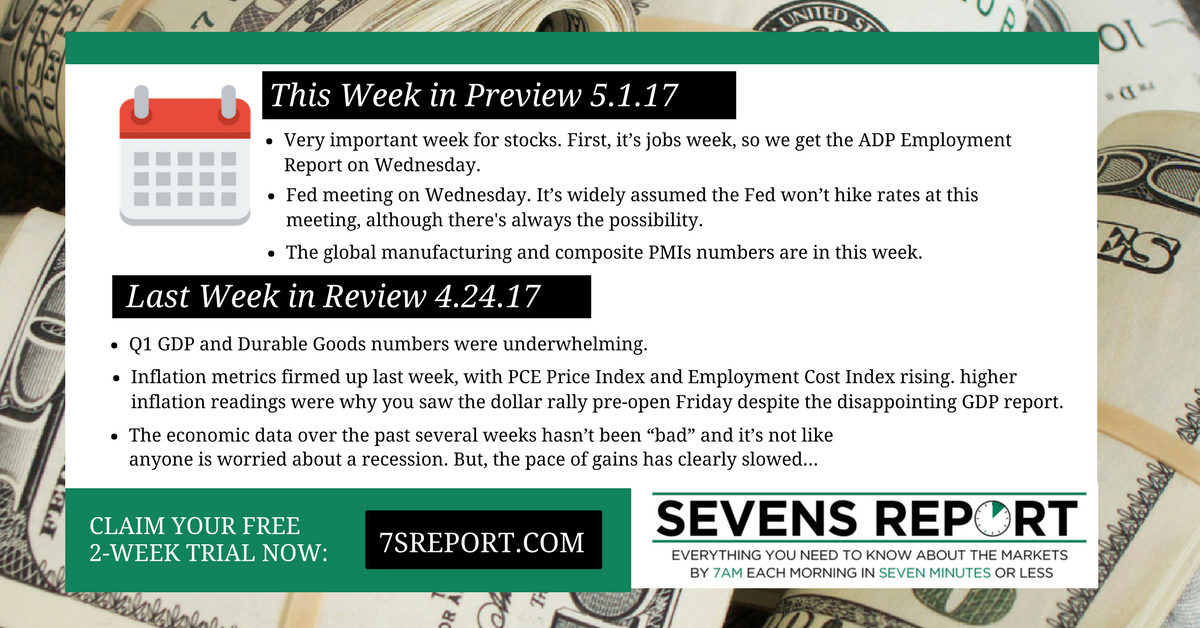

Looking at the headliner from last week, Q1 GDP, it was underwhelming, as expected. Headline GDP was just 0.7% vs. (E) 1.1%, and consumer spending (known as Personal Consumption Expenditures or PCE) rose a mea-sly 0.3%. But, the 0.7% headline met the soft whisper number and that’s why stocks didn’t fall hard on Friday.

That GDP report came on the heels of another underwhelming Durable Goods number. The headline missed estimates but the more importantly, New Orders for Non-Defense Capital Goods ex-Aircraft rose just 0.2% vs. (E) 0.4%, although revisions to the February data were positive.

Meanwhile, inflation metrics firmed up last week. First, the PCE Price Index in Friday’s GDP report rose 2.2% vs. (E) 2.0%, while the Employment Cost Index, a quarterly gauge of compensation expenses, rose 0.8% in Q1 vs. (E) 0.4%. Those higher inflation readings were why you saw the dollar rally pre-open Friday despite the disappointing GDP report.

Bottom line, the economic data over the past several weeks hasn’t been “bad” and it’s not like anyone is worried about a recession. But, the pace of gains has clearly slowed, and until we see a resumption of the economic acceleration many analysts were expecting at the start of 2017, any material stock rally from here will not be economically or fundamentally supported (and remember, it was the turn in economic data back in August/September that ignited the late 2016 rally. Yes, the election helped, but the momentum was positive before that event, so economics do matter).

This Week in Economics – 5.1.17

Economic data this week could go a long way towards helping to resolve the large gap between soft sentiment surveys and hard economic data, given the large volume of economic reports looming this week.

First, it’s jobs week, so we get the ADP Employment Report on Wednesday and the official jobs report on Friday. We’ll do our typical “Goldilocks Jobs Report Preview” on Thursday, but after March’s disappointing jobs number, the risks to this report are more balanced (it could easily be too hot if the number is strong and there are positive revisions, or it could be too cold and further fuel worries about the pace of growth).

Second in importance this week is the Fed meeting on Wednesday. The reason this is second in importance is because it’s widely assumed the Fed won’t hike rates at this meeting (June is the next most likely date for a rate hike), although the Fed has turned slightly more hawkish so there’s always the possibility. We’ll send our FOMC Preview in Wednesday’s report but the wildcard for this meeting is whether the Fed gives us any more color into how it plans to reduce its balance sheet. If the Fed does reference or start to explain how its plans to reduce its balance sheet, that could be a hawkish surprise for markets.

Finally, we get the global manufacturing and composite PMIs this week. Most of Europe is closed today for May Day so just the US ISM Manufacturing PMI comes today, with the European and Japanese numbers out tomorrow. Then, on Wednesday, we get the US Service Sector PMI and global composite PMIs on Thursday. The global numbers should be fine but the focus will be on the US data. In March we saw a loss of positive momentum in these indices but the absolute levels of activity remained healthy. If we see more moderation and declines in the ISM Manufacturing and Non-Manufacturing PMIs in April, that will stoke worries about the overall pace of growth in the economy and that will be a headwind on stocks.

Bottom line, this a pretty pivotal week for the markets. On one hand, if economic data is strong and the Fed a non-event, the S&P 500 could push and potentially break-through 2400. Conversely, if economic data is underwhelming and the Fed mildly hawkish, we could easily see last week’s earnings/French election rally given back, and the S&P 500 could fall back into the middle of the 2300-2400 two months long trading range.

The Sevens Report is your weekly cheat sheet. Get a free two-week trial: 7sReport.com.

")

")