FOMC Meeting Takeaways, August 17, 2017

The Sevens Report is everything you need to know about the markets in your inbox by 7am, in 7 minutes or less. Start your free two-week trial today and see what a difference the Sevens Report can make.

The FOMC minutes resulted in a “dovish” reaction in currencies and bonds, but in reality they didn’t reveal anything new.

Takeaway

The two big takeaways from Wednesday’s FOMC were 1) The Fed is united in reducing the balance sheet in September (which will be the start of the removal of additional accommodation) and 2) The Fed is divided on whether to hike rates in December because of low inflation. Neither of those takeaways should be surprising to anyone who has been paying attention.

The former (that the Fed is committed to reducing its balance sheet) was reaffirmed by the minutes yesterday, and while the market seems to be ignoring this event, I do want to remind everyone that the Fed will be reducing its Treasury holdings for the first time in a decade. That will, over time, have a “tightening” effect on the economy (although admittedly not at first).

The latter was where the market generated it’s “dovish” interpretation of the Fed minutes, but in reality the fact that “some” Fed members want to not hike rates again this year shouldn’t be a surprise. Bullard, Kashkari, Mester and others have voiced caution about further rate hikes in the past few weeks due to low inflation.

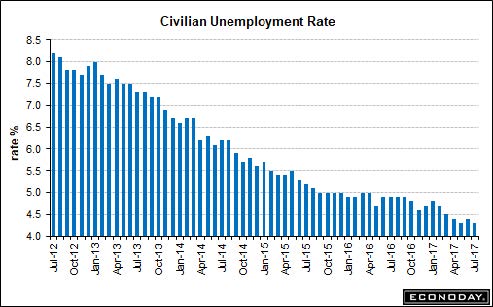

Conversely, Dudley, Williams and others have stressed very low unemployment and still-loosening financial conditions as reasons to continue with gradual rate increases. Otherwise, they risk getting behind a sudden upshot in inflation that forces them to raise rates very quickly.

Point being, we know there is this divide, and it will be resolved in the coming months based on inflation data. If inflation data bottoms and heads higher, they’ll hike rates in December. If it doesn’t, they probably won’t. That’s no different than it was Wednesday at noon.

From a market standpoint, the reaction was “dovish” as the dollar and bond yields dropped, and stocks rallied modestly. But, yesterday’s FOMC minutes should not be enough to elicit a material rally in stocks, nor should it be enough to push the dollar or bond yields to recent 2017 lows.

About the only notable takeaway from the minutes is that it’s likely anecdotally bullish for the “Stagnation” portfolio…(withheld for subscribers only—unlock specifics and ETFs by signing up for a free two-week trial).

Time is money. Spend more time making money and less time researching markets every day. Subscribe to the 7sReport.com.