Crude Oil Prices May Impact Inflation

Crude Oil Prices May Impact Inflation: Tom Essaye Quoted in Forbes

Lockheed Martin, Northrop Grumman Stocks Notch Best Days In Years Amid Israel-Hamas Conflict

Defense stocks surged while the broader market dipped Monday as Wall Street sifted through the market fallout of the conflict between Israel and Hamas, which escalated this weekend by the latter’s historic attack.

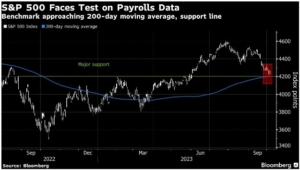

Sevens Report analyst Tom Essaye attributed this early slump to “rising geopolitical tensions,” pointing to how the related surge in crude oil prices may impact inflation and thus could keep monetary policy tighter.

Also, click here to view the full Forbes article published on Octobe 9th, 2023. However, to see the Sevens Report’s full comments on the current market environment sign up here.

If you want research that comes with no long term commitment, yet provides independent, value added, plain English analysis of complex macro topics, then begin your Sevens Report subscription today by clicking here.

To strengthen your market knowledge take a free trial of The Sevens Report.

Join hundreds of advisors from huge brokerage firms like Morgan Stanley, Merrill Lynch, Wells Fargo Advisors, Raymond James, and more! To start your quarterly subscription and see how The Sevens Report can help you grow your business, click here.