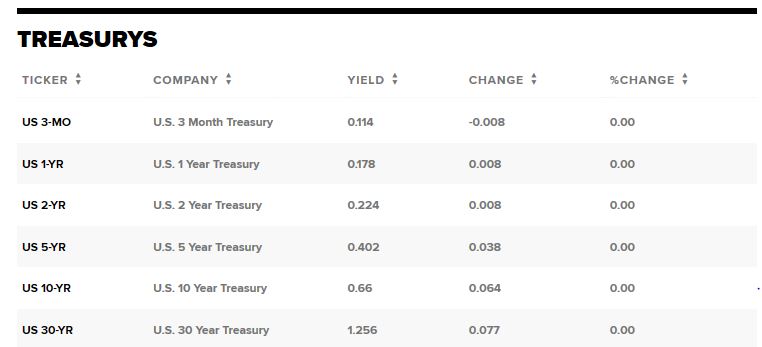

What’s in Today’s Report:

- Sevens Report Economic Breaker Panel – April Update

Futures are decidedly lower with global markets this morning as optimism for a V-shaped economic recovery fades ahead of key economic data and more important earnings today.

Additionally, Trump cut funding to the WHO, raising tensions with China while WTI crude oil prices fell to fresh 18-year lows, below $20/barrel, overnight as a complete lack of demand continues to weigh on the broader energy markets right now.

Looking into today’s session, it is lining up to be a busy one from a potential catalyst standing.

First, there are several important economic reports due to be released including: Retail Sales (E: -7.0%), Empire State Manufacturing Survey (E: -35.0), Industrial Production (E: -4.2%), and the Housing Market Index (E: 60) while there is one Fed official schedule to speak: Bostic (1:00 p.m. ET).

Earnings will also be a major focus today with Q1 results due out from: BAC ($0.65), C ($1.83), GS ($2.83), PNC ($2.24), USB ($0.87), PGR ($1.44), and BBBY ($0.21).

Stocks have become near-term overbought over the last few weeks so any notably negative news flow regarding economic data, earnings, or the coronavirus pandemic could cause a potentially volatile wave of profit taking.