What’s in Today’s Report:

- Vaccine Playbook (Results Hopefully Coming Next Week)

- September Durable Goods Orders Takeaways

- Consumer Confidence Miss (Chart)

Stock futures are tracking global shares lower this morning with European markets hitting multi-month lows as coronavirus cases continue to surge and multiple governments, including France and Germany, discuss new lockdowns.

There were no notable economic reports overnight and the only report in the U.S. today is: International Trade in Goods (E: -$85.0B).

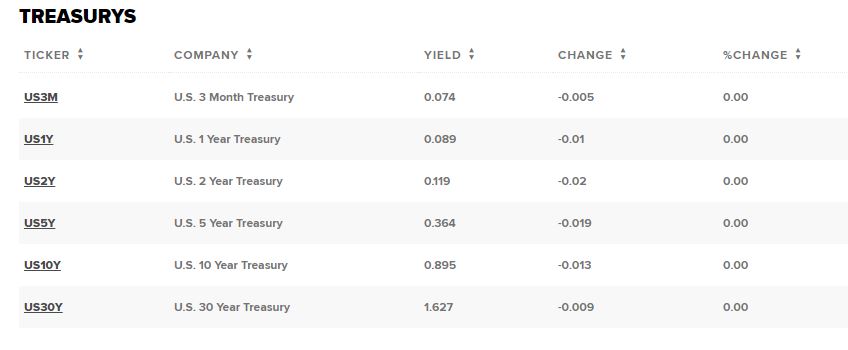

There are no Fed speakers scheduled to speak today however the Treasury will hold a 5-Yr Note Auction at 1:00 p.m. ET, and given the fact that the yield curve has come into focus recently with the 10s-2s spread near 2020 highs, any material impact the auction has on the yield curve could impact stocks (new highs would be negative right now)

Finally, earnings season remains in full swing with: BA (-$2.33), UPS ($1.86), GE (-$0.06), and MA ($1.65) reporting ahead of the bell while V ($1.09) and F ($0.22) will release Q3 results after the close.

The recent resurgence in global COVID-19 cases and subsequent moves by multiple major governments to revert to lockdown measures to combat the spread of the virus has taken over as the main influence on risk assets right now, especially with hopes for a pre-election stimulus deal effectively dead at this point.

So today, the market’s main focus will be on the latest outbreak statistics and various governments policy reactions, especially in the U.S. And if we see renewed lockdowns implemented in various hotspots, then stocks could extend this week’s selloff, potentially in a big way.