Jobs Report Preview (Higher “Too Hot” Limits)

Jobs Report Preview (Higher “Too Hot” Limits): Start a free trial of The Sevens Report.

What’s in Today’s Report:

- Jobs Report Preview (Higher “Too Hot” Limits)

Futures are little changed ahead of the jobs report and following a mostly quiet night of news.

Tech earnings were mixed as semi-conductor/AI linked stocks AVGO and MRVL earnings underwhelmed and both stocks are lower pre-market (-2% and -5% respectively).

Economically, ECB member Francois de-Villeroy said a rate cut in April or June is “very likely” further reinforcing expectations for summer rate cuts from global central banks.

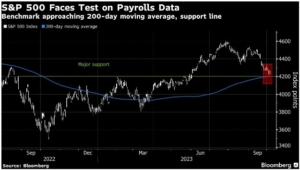

Today focus will be on the jobs report and expectations are as follows: 190K Job Adds, 3.7% Unemployment Rate, 0.3%/4.3% Wage Growth. Powell and other Fed members sound committed to rate cuts barring a bounce back in inflation so for the jobs number to be “Too Hot” we’ll need to see strong job adds, wage gains and low unemployment. Barring “hot” numbers across those metrics, the jobs report likely won’t materially reduce June rate cut expectations. If it does, however, expect a real uptick in volatility.

Finally, there’s one Fed speaker today, Williams at 7:00 a.m. ET, but he shouldn’t move markets.

Join hundreds of advisors from huge brokerage firms like Morgan Stanley, Merrill Lynch, Wells Fargo Advisors, Raymond James, and more! To start your quarterly subscription and see how The Sevens Report can help you grow your business, click here.