The Economy: A Look Back and What’s Ahead

Last Week

The most important thing that happened last week economically was that expectations for Fed tapering of QE were pulled forward a bit—from the previous “consensus” of mid-2014 to the early part of 2014— thanks mainly to an FOMC statement that wasn’t as “dovish” as expected plus a Jon Hilsenrath sentence that stated a December taper remains “on the table.” Interestingly, this change in expectation came despite decidedly mixed economic data.

Starting with the FOMC statement from last Wednesday, it seems most are calling it slightly “hawkish,” but that’s really only because it didn’t feature any material downgrade of the economy in the commentary (as was widely expected).

Looking at the actual statement, it was hardly changed from September, although the two important takeaways were that the FOMC noted the labor market had slid a bit and also somewhat celebrated that interest rates had declined.

Both changes are, on balance, slightly “dovish.” So even though the market didn’t trade that way, I think the meeting didn’t really change anything with regard to when the Fed will taper QE (and certainly didn’t materially pull it forward, as they remain data-dependent).

Outside of the FOMC, as I said, economic data was at best mixed. Early in the week, things looked somewhat grim:

- The manufacturing indicator of the September industrial production report was weak and August was revised down.

- Pending home sales dropped 5.6%, the biggest monthly drop since April 2011.

- The October ADP employment report missed expectations at just 130K jobs added, and the September figure was revised lower as well.

These reports were especially disconcerting because they implied the economy was seeing a slowing of growth before the government shutdown, as this data was from before October.

Later in the week, though, the data surprisingly turned better. Chicago PMI, which isn’t usually a watched number, caught people’s attention. It exploded to a multi-year high, and the details of the report were equally strong. And, on Friday, the national ISM manufacturing PMI increased 0.2 to 54.4, beating expectations of a small decline. So, if anything, the beginning of the week was considered “dovish” but turned “hawkish” as the week went on.

I’m spending time talking about how the market interprets the data (hawkishly or dovishly) because right now it’s as important as the actual data itself. As was the case prior to the government shutdown, the question of “When will the Fed taper QE?” remains the single biggest driving factor in the markets (for bonds, the dollar, commodities and equities).

The first three assets have traded (and will trade more immediately) to shifting “tapering” expectations, as we saw last week. But, although stocks won’t trade off daily shifting of tapering expectations, it very much remains to be seen if stocks can rally in a “QE-less” world.

Ultimately, if the Fed has to taper QE and the economy isn’t very strong, that could usher in “stagflation” and be a rally-killer. So when and how this whole thing works out remains the key to any medium-term outlook for equities.

This Week

There aren’t many economic releases this week, but the October jobs report is Friday and clearly that’s important from a WWFD (What Will the Fed Do?) standpoint, although this jobs report will be taken with a hefty grain of salt given the government shutdown.

Also on Friday is the “Personal Income and Outlays” report, which is particularly important because it gives us a look at the Fed’s preferred measure of inflation—the core Personal Consumption Expenditures deflator. Stubbornly low inflation has been a growing concern of the Fed’s for some time, so a weak core PCE deflator will be “dovish.”

Also on the calendar this week is the first look at Q3 GDP on Thursday (expectations are for close to 2%), weekly jobless claims (this report will be overshadowed by the October report Friday) and ISM Non-Manufacturing (or service sector) PMIs (Tuesday). Really, though, those reports won’t move the needle much with regard to WWFD. (GDP is more a media favorite than anything anyone really trades off of.)

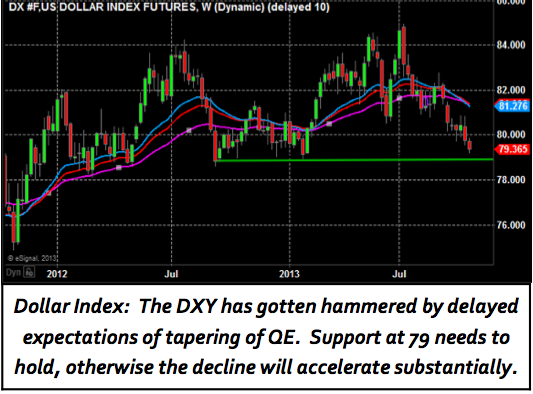

Outside of the jobs report, arguably the other “highlight” of the week will be the ECB meeting Thursday. The euro plunged last week (and the Dollar Index spiked) on a very weak inflation reading, and speculation is high as to whether the ECB will cut rates to fend off a hint of deflation potentially hitting the “Continent.” Given the falling euro’s effect on the Dollar Index, this meeting has implications for the commodity markets particularly.