Last Week

The actual economic data released last week were at best just “ok,” but that was overshadowed by the various statements, actions and expectations of the major global central banks. Markets were reminded that global central bank policy remains very easy (and will likely in aggregate get more accommodative in the future).

The biggest economic event last week was supposed to be a non-event, and that was the BOJ meeting. By now you know that the BOJ announced plans to increase its QE program by 30 trillion yen (to 80 trillion per year), triple the purchases of J-REITs and ETFs, and double its stock holdings. Additionally, the Japanese Government Pension Investment Fund made official expected major allocation changes, which will see domestic bond holding cut dramatically in favor of increased allocations to domestic and foreign equities and foreign bonds. This news, as you know, was the reason for the big rally Friday.

In an impressive feat, the BOJ shocker almost made markets forget that the Fed ended QE here in the U.S. (as expected). But, the Fed also provided some surprise through the statement, which reflected a slightly “hawkish” tone. The FOMC significantly upgraded their commentary toward the labor market and downplayed the recent drop in CPI as mostly a temporary, commodity-led phenomenon.

But, while the statement was more “hawkish” than expected, it’s important not to get lost in the details. Bottom line, on the margin we need to look at the FOMC as more committed to rate increases at some point in the future (which is good), but they remain very, very accommodative.

Finally, the ECB was quiet last week, but they did announce they will start buying Asset-Backed Securities in November. Meanwhile, the economic data in Europe added more pressure for the ECB to do “more” via buying corporate bonds or outright QE.

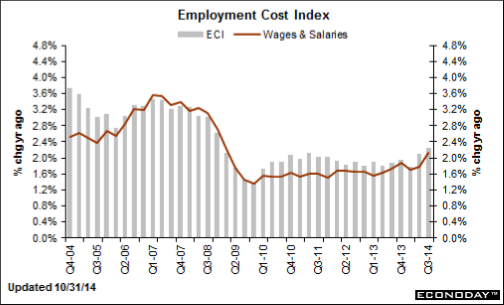

Specifically, the October “flash” HICP (the EU CPI) was again subdued, rising 0.4% month-over-month but more importantly the “core” reading declined to a 0.7% increase year-over-year from 0.8% in September. Bottom line, deflation remains a major threat in the EU, and data are continuing to increase the chances of the ECB doing “more” to achieve its balance sheet expansion targets.

Turning to the actual data, in the U.S. it was lackluster, as mentioned. September Durable Goods was a bad number, as was New Orders of Non-Defense Capital Goods Excluding Aircraft (NDCGXA), which is the sub-index to watch in this release, fell 1.7%. This suggests some softening of the manufacturing sector in September, likely due to reduced exports courtesy of the stronger dollar.

Finally, the first look at Q3 GDP was better than expected at 3.5% vs. (E) 3.0%. It was a good number but the headline was deceiving. A big uptick in government spending (thanks to the ISIS campaign) and a reduction in imports (which normally subtract from GDP) were responsible for much of the “beat.”

This Week

Global growth and inflation remain the two areas to watch from a macro standpoint. Last week we got a lot of data on inflation (which seems ok everywhere except Europe) while this week we get a lot of data on growth.

The most important number this week, as usual, is the October jobs report. And, it’s also “jobs week” so we should expect ADP Wednesday, claims Thursday and the government number Friday. Again, unless this is a materially bad number, don’t expect it to change anyone’s outlook on stocks or the economy.

We already got the official global manufacturing PMIs (the Chinese data slightly missed at 50.8 vs. 51.2 and will keep alive concerns about the pace of growth), while German and EMU PMIs also slightly missed, but stayed above 50 (reflecting a still fragile economy). U.S. manufacturing PMIs come later this morning.

Later this week we get the global composite PMIs (both manufacturing and services), with China releasing data Tuesday night, Europe Wednesday morning and the U.S. “Non-Manufacturing” or services PMI later Wednesday morning.

Domestically other than the aforementioned numbers it’s pretty quiet. The same can’t be said for Europe, though, as there is an ECB meeting Thursday. Although no changes to policy are expected, as the BOJ showed last week, anything is possible.

Bottom line this week is it’s important to keep the data in the context of the last three weeks. Remember concerns about global growth were at the heart of the recent sell-off, but that stopped two weeks ago when flash PMIs were better than expected. At this point, global growth being “better than feared” is priced into stocks, so the risk this week is for a negative disappointment from the data.

To continue reading today’s Sevens Report, simply sign up for a Free Trial on the right hand side of this page.