What’s in Today’s Report:

- What Makes a Vaccine a Bullish Gamechanger?

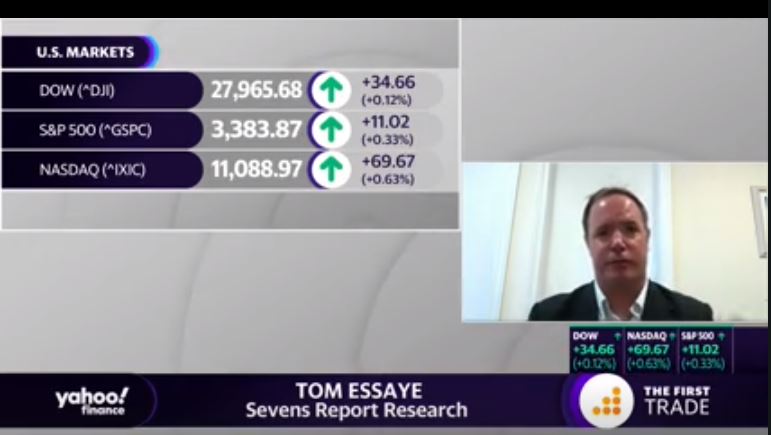

Stock futures are rallying this morning suggesting that the S&P 500 will open at a fresh record high today while global shares rose overnight on easing geopolitical tensions.

Late yesterday, high-level officials from the U.S. and China including Secretary Mnuchin and Vice Premier Liu He held a “constructive” virtual meeting during which both sides reiterated commitment to the Phase-One trade deal.

Economic data largely met expectations overnight and did not materially affect markets with a focus on improving relations between the U.S. and China.

Looking into today’s session, the focus will remain on the apparent progress on trade between the U.S. and China however there are a few additional catalysts to watch.

Economically, we will get three reports on the housing market: Case-Shiller House Price Index (E: 0.1%), FHFA House Price Index (E: 0.3%), and New Home Sales (E: 774K) but Consumer Confidence (E: 93.0) will be the most important release to watch (it hits shortly after the bell at 10 a.m. ET).

There is also one Fed speaker late in the day: Daly (3:25 p.m. ET). Beyond that, the market will remain sensitive to any news regarding the Congressional stalemate over the stimulus bill and any new progress will be well received by markets.