The Sevens Report is the daily market cheat sheet our subscribers use to keep up on markets, leading indicators, seize opportunities, avoid risks and get more assets. Get a free two-week trial with no obligation, just tell us where to send it.

Last Week in Review:

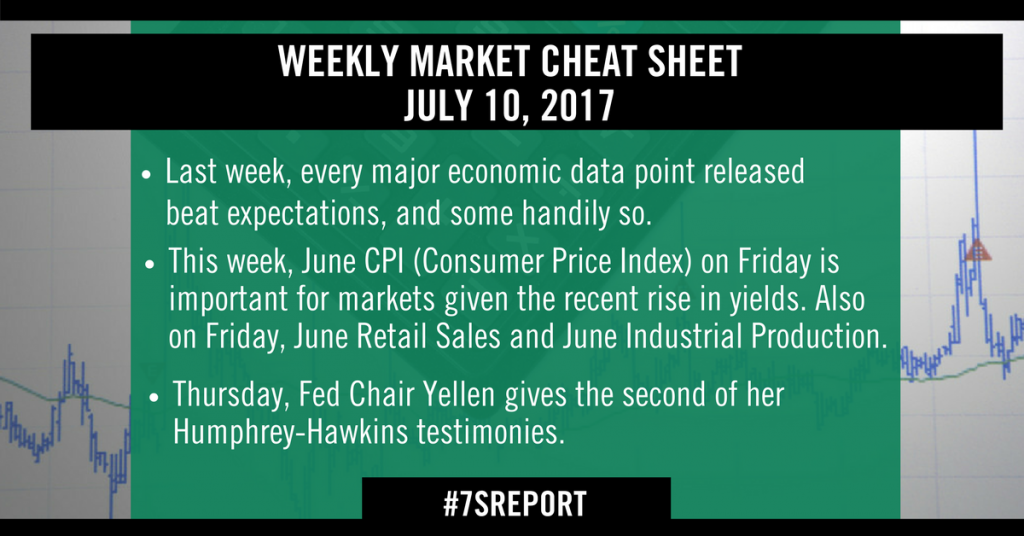

Reflation on? Not just yet, but last week’s data did imply that the US economy may be starting to gain more positive momentum, which will be much to the Fed’s relief after looking past recent soft economic data. Specifically, every major economic data point released last week beat expectations, and some handily so.

Before getting to those numbers, it’s important to address the biggest market-moving event last week: The ECB meeting minutes. Anticipation of those minutes, which were mildly hawkish, caused the German bund yield to break to a multi-year high above 0.5%, and that caused an acceleration in the decline in bonds/rise in yields that ultimately resulted in the 1% decline in stocks last Thursday.

The importance of the ECB minutes (and largely all the data from last week) was that it confirmed central banks do expect better growth and inflation, and that expectation is leading them to get less dovish, which is sending global bond yields higher.

The bottom line for the ECB and the Fed remains 1) The ECB is expected to begin to taper QE in January 2018, and end it completely in mid-2018, while the Fed is expected to begin to reduce the balance sheet in September, and hike rates again in December. The events of this week reinforced those expectations, which are largely priced into stocks and bonds at this point.

Turning to the economic data, it was good last week. The jobs report was the highlight, and it was strong. Job adds in June were 222k, solidly above the 170k estimate. However, wages were a slight disappointment, up just 0.2% and 2.5% yoy, which stopped the strong jobs report from being “Too Hot.”

Looking at the other two key numbers last week, the June ISM Manufacturing PMI and ISM Non-Manufacturing PMI, they also were strong. The Manufacturing PMI surged to the best level since August 2014, rising to 57.8 vs. (E) 55.1 while the Non-Manufacturing (or service sector) PMI rose to 57.4 vs. (E) 56.5. Details of both reports were also strong, as New Orders rose, suggesting continued momentum into the summer.

To a point, the data can be taken with a grain of salt, because there’s no question the jobs market remained strong in June (the weekly claims told us that) while the PMIs are still just “soft data” in so much as it’s survey data, and not hard economic data. Still, these numbers were good, and it does reinforce that we are seeing an emerging reflation in the economy, and an emerging reflation trade in markets.

This Week’s Preview:

Normally after the jobs report the following week is pretty quiet on the economic front. Yet that’s not so this week, as we get three very important economic numbers Friday.

June CPI is the highlight of the week, and it will be an important number for markets given the recent rise in yields. Since the Fed and other global central banks expressed surprising confidence in their respective economies in June, economic data has largely reinforced that expectation.

However, now it’s inflation’s turn. If inflation metrics show a further loss of momentum, that will undercut central bank’s expectation of future inflation, and could cause at least a mild reversal in the recent reflation trade (so bond yields down, banks/small caps/cyclicals down, defensives/tech up). Conversely, if CPI is strong, it will further prove central banks were right to look past the soft data, and the reflation trade will likely accelerate. So, this will be an important number regarding sector trade, and near-term performance in the broad market.

Also on Friday we get June Retail Sales and June Industrial Production. As previously mentioned, there is still a gap between soft, survey-based data (the PMIs) and hard, actual economic numbers. Given the strength in the PMIs, expectations for better actual economic data via Retail Sales and Industrial Production now is somewhat expected.

Finally, Fed Chair Yellen gives the second of her Humphrey-Hawkins testimonies this week, and she will address the Senate Banking Committee on Wednesday and the House Financial Services Committee Thursday. The tone of her comments will obviously be closely watched, but with several years on the job, Yellen seems to have learned not to give anything away in these testimonies. Yet if her tone echoes the confidence in the economy and inflation that we saw in the June FOMC meeting, it will be at least a mild reinforcement of the reflation trade across assets (i.e. higher yields).

Get the simple talking points you need to strengthen your client relationships with the Sevens Report. Everything you need to know about the markets delivered to your inbox by 7am each morning, in 7 minutes or less.

President Trump, in an interview with the WSJ yesterday, appeared to change his policy on the Fed and interest rates. Specifically, Trump said he thought the dollar was getting too strong, that he favored a low interest rate policy, and he was open to keeping Yellen as Fed Chair. It was the second two comments that caught markets attention and caused a “dovish” response in the dollar and bond yields (both of which fell).

President Trump, in an interview with the WSJ yesterday, appeared to change his policy on the Fed and interest rates. Specifically, Trump said he thought the dollar was getting too strong, that he favored a low interest rate policy, and he was open to keeping Yellen as Fed Chair. It was the second two comments that caught markets attention and caused a “dovish” response in the dollar and bond yields (both of which fell).