A True Curve Inversion

What’s in Today’s Report:

- When Is a Yield Curve Inversion Truly a Negative Signal

- Consumer Confidence Takeaways (Hawkish Risks)

It is another quiet morning with mixed price action as stock futures edged higher on positive Italian political headlines while Treasury yields extend recent losses despite the lack of any material economic releases or trade headlines.

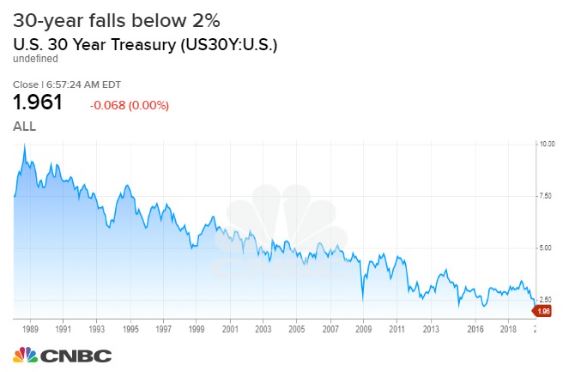

In the bond market, the benchmark 10s-2s yield curve spread hit a fresh 12 year low below -5 basis points this morning while the 30-Year yield has hit a new record low, signaling more broad market angst by the “smart market.”

Looking into today’s session, there are no economic reports although the EIA will release weekly oil and refined product inventory statistics at 10:30 a.m. ET and after last night’s 11.1M bbl draw reported by the API, we could see significant moves in the oil market today and that could affect stocks.

As far as other catalysts go, there is one Fed speaker today: Daly but not until after the closing bell (5:30 p.m. ET) while there is also a 5-Year T-Note Auction (1:00 p.m. ET) which could move yields and ultimately stocks.

Lastly, U.S.-China trade talks were scheduled for the front half of this week and so far there has not been any news on the topic. But, investors will continue to wait for any new developments on the trade war front as it is the primary influence on global markets right now.