Tom Essaye Interviewed on Schwab Network

American Express (AXP) rises after beating earnings: Tom Essaye Interviewed on Schwab Network

AXP Rises After Earnings: Best Positioned Credit Card Stocks

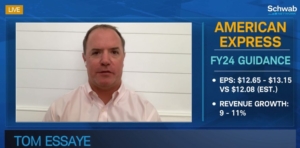

American Express (AXP) rises after beating earnings. The Sevens Report’s Tom Essaye and Morningstar’s Michael Miller discuss this as American Express’ 1Q revenue grew 11% year-over-year. They talk about the road ahead for American Express. They then go over the best positioned credit card stocks. Tune in to find out more about the stock market today.

Also, click here to view the full interview published on April 19th, 2024. However, to see the Sevens Report’s full comments on the current market environment sign up here.

To strengthen your market knowledge take a free trial of The Sevens Report.

Join hundreds of advisors from huge brokerage firms like Morgan Stanley, Merrill Lynch, Wells Fargo Advisors, Raymond James, and more! To start your quarterly subscription and see how The Sevens Report can help you grow your business, click here.