Tom Essaye and Yahoo Finance Opening Bid Panel Discuss Big Banks

I think that this is a very smart move by Meta, Says Tom Essaye

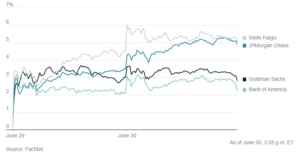

Big banks see consumer holding up despite economic uncertainty

Yahoo Finance Executive Editor Brian Sozzi and his Opening Bid panel featuring guests: Globalt Investments senior portfolio manager Thomas Martin, Sevens Report Research founder Tom Essaye, and Yahoo Finance Senior Business Reporter Brooke DiPalma discuss what big banks are saying about consumer resiliency.

As long as the unemployment rate stays low. That’s the key to the whole sort of economic resiliency. That and the fact that the hyperscalers are just fire hosing hundreds of billions of dollars into all corners of the economy as they build out data centers as fast as they can. But the unemployment rate is low

And people can get jobs. And as long as that’s the case, then they’re going to be generally able to keep up, relatively speaking, with this inflation, and that’s been the key. The trouble is if that unemployment rate starts to rise or that people start to have a hard time finding jobs. That’s the lynch pin. As long as the unemployment rate stays low, then people can continue to stomach very high beef prices and egg prices and all the other things we’re having to deal with.

Also, click here to view the full video published on Yahoo Finance on July 14th, 2026. However, to see the Sevens Report’s full comments on the current market environment sign up here.

If you want research that comes with no long term commitment, yet provides independent, value added, plain English analysis of complex macro topics, then begin your Sevens Report subscription today by clicking here.

To strengthen your market knowledge take a free trial of The Sevens Report.

Join hundreds of advisors from huge brokerage firms like Morgan Stanley, Merrill Lynch, Wells Fargo Advisors, Raymond James, and more! To start your quarterly subscription and see how The Sevens Report can help you grow your business, click here.