Tom Essaye Quoted in Barron’s on September 24, 2019

“Futures are higher with most overseas markets thanks to positive trade headlines…” writes the Sevens Reports’ Tom Essaye. Click here to read the article.

“Futures are higher with most overseas markets thanks to positive trade headlines…” writes the Sevens Reports’ Tom Essaye. Click here to read the article.

What’s in Today’s Report:

Stock futures are extending losses this morning and international equity markets were broadly lower overnight as political and trade uncertainties weigh on sentiment.

Speaker of the House, Nancy Pelosi, formally announced an impeachment inquiry regarding President Trump’s interactions with the President of Ukraine which has added to an already crowded list of potential market headwinds.

Otherwise, it was a relatively quiet night of news with no material economic data releases and no trade war developments.

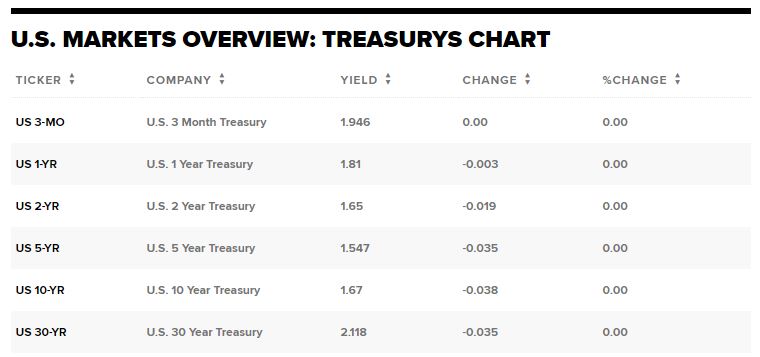

Today, there is one economic report to watch: New Home Sales (E: 665K) and a relatively busy schedule of Fed speakers: Evans (8:00 a.m. ET), George (10:00 a.m. ET), and Kaplan (7:00 p.m. ET). There is also a 5-Yr Treasury Note Auction at 1:00 p.m. ET and based on yesterday’s very solid 2-Yr Auction that helped steepen the yield curve, the results could once again influence the stock market.

Beyond those scheduled market catalysts, investors will be focused on the fluid impeachment situation as well as sensitive to any trade war developments.

“Gold has fallen into a broad, near-term trading range between support at $1,500 and resistance above at $1,560. There are multiple influences on gold right now that could trigger…” said Tyler Richey, co-editor at Sevens Report Research. Click here to read the full article.

“These are not good numbers and they do not imply global economic stabilization is occurring,” said Tom Essaye, founder of The Sevens Report, in a note. Click here to read the full article.

What’s in Today’s Report:

Futures are higher with most overseas markets thanks to positive trade headlines and easing Brexit concerns.

Treasury Secretary Mnuchin said last night that Chinese Vice Premier Liu He will travel to Washington for high level trade negotiations in two weeks and that China has encouragingly made significant agricultural purchases so far this week.

British courts ruled the suspension of Parliament by Boris Johnson unlawful, reducing odds of a no-deal Brexit.

Today, there are a few economic reports to watch: S&P Case-Shiller HPI (E: 0.1%), FHFA House Price Index (E: 0.2%), and Consumer Confidence (E: 133.6) and no Fed speakers are scheduled to speak.

There is however a 2-Yr Treasury Note auction at 1:00 p.m. and the results have recently led to sizeable moves in the bond market and subsequently influenced stocks, so there is a potential for volatility in the early afternoon.

And maybe that’s because there’s still so much uncertainty out there regarding trade? Yes, the U.S. has exempted more than 400 goods from tariffs, and come as both the two sides get ready for October negotiations. “On U.S./China trade, the staffer meeting in preparation for the October meeting will continue, and absent any ‘real’ news today any chatter that’s positive on…” writes The Sevens Reports’ Tom Essaye. Click here to read the full article.

Stocks quickly rolled over Thursday after the comments came to light, finishing near the lows of the session. As Sevens Report Research founder Tom Essaye wrote to clients, the algos that scan the internet for headlines took control after Pillsbury’s comments. The machines were right to…Click here to read the full article.

What’s in Today’s Report:

Futures are flat as economic data was weak, but countering that was positive comments on U.S./China trade.

September EU flash composite PMIs were ugly, as the headline dropped to 50.4 vs. (E) 52.0 while manufacturing fell to 45.6 vs. (E) 47.3. As usual, U.S./China trade is over shadowing everything else, but these are not good numbers and they do not imply global economic stabilization is occurring.

On U.S./China trade, the Chinese Ministry of Finance called last week’s talks “constructive” and that’s alleviating fears the earlier than expected departure implied a breakdown.

Today the key number is the Sept. Flash PMI (E: 51.2) and it needs to meet or beat expectations, otherwise concerns will continue to rise about the future growth of the U.S. economy.

There are also three Fed speakers (Williams (9:50 a.m.), Bullard (1:00 p.m.), Daly (2:30 p.m.)) we got a lot of Fed speak on Friday and it didn’t change the current outlook, so there’s no reason to think that will happen today.

The report also showed that U.S. oil output held steady last week at 12.4 million barrels a day, just 100,000 barrels a day less than the all-time high reached last month… said Tyler Richey, co-editor of Sevens Report Research. Click here to read the full article.

What’s in Today’s Report:

Futures are marginally higher after China cut interest rates, although the cut was less than expected.

China cut its Loan Prime Rate (LPR) by five basis points. The rate cut was expected but it was supposed to be a 10-15 basis point cut, so the action isn’t as strong as hoped for and Chinese economic growth will remain a concern.

Economic data was sparse overnight as Japanese CPI met expectations at 0.5% yoy.

Today there aren’t any economic reports but there are several Fed speakers, including Bullard who already spoke and was dovish (which isn’t a surprise, he wanted a 50 bps cut this week). The most important speaker today is Williams (8:15 a.m. ET) as he’s considered part of Fed leadership, and if he advocates for more cuts that’ll be a dovish tailwind on stocks. Other speakers today include Rosengren (11:20 a.m. ET) and Kaplan (1:00 p.m. ET).

On U.S./China trade, the staffer meeting in preparation for the October meeting will continue, and absent any “real” news today any chatter that’s positive on U.S./China trade and/or dovish will help stocks rally.