What’s in Today’s Report:

- Yield Curve Update: Historically Speaking

U.S. equity futures are up more than 1% this morning, recovering the bulk of yesterday’s late afternoon declines amid continued hopes for a looming economic recovery.

Economically, Japanese Machine Orders for March declined -0.4% after rising 2.3% in February while inflation statistics in Europe were on the soft side, but none of the data materially moved markets overnight.

There are no notable economic reports today however the Treasury will hold a 20-Year Bond Auction at 1:00 p.m. ET, and as we have seen so far this year, any resulting move in yields (specifically the curve) could influence equity market trading.

There are also a few potential Fed catalysts today with two speakers on the schedule: Bostic (10:00 a.m. ET) and Bullard (12:00 p.m. ET), and the release of the FOMC meeting minutes at 2:00 p.m. ET.

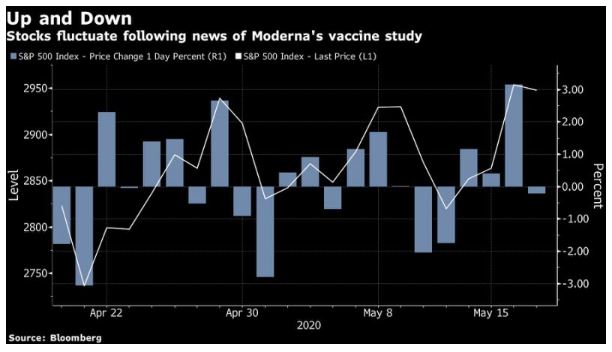

The market remains primarily focused on the still very fluid coronavirus outbreak situation and economic reopening process, as well as any further developments about vaccines or treatments. Any positive headlines, specifically regarding the latter, could help power stocks to fresh multi-week highs today, while contrarily, negative news could see a repeat of yesterday’s late day selloff.