Tom Essaye Quoted in Fintech Zoom on March 5, 2021

“While the S&P 500 may be facing structural head-winds due to tech weakness, much of the rest…” Tom Essaye, founder of Sevens Report, said according to CNBC. Click here to read the full article.

“While the S&P 500 may be facing structural head-winds due to tech weakness, much of the rest…” Tom Essaye, founder of Sevens Report, said according to CNBC. Click here to read the full article.

What’s in Today’s Report:

Futures are moderately lower despite stimulus progress over the weekend, as markets digest Friday’s big rally.

The Senate passed the $1.9 trillion stimulus bill and the House will debate it on Tuesday. Biden could sign the bill by the end of the week, meeting market expectations and unleashing more stimulus into the economy as we begin the 2nd quarter.

Economically, Chinese trade numbers signaled an ongoing global recovery as exports exploded 60.6% y/y vs. (E) 40%.

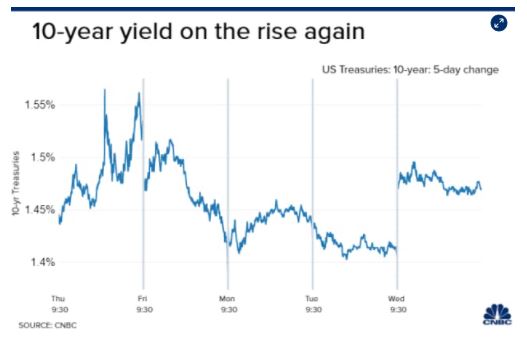

The 10 year Treasury yield is up four basis points on the stimulus news and is again testing 1.60% (this is the main reason futures are lower this morning).

Today there are no economic reports and no Fed speakers, but yields will once again dictate trading in stocks. Markets rallied on Friday because the 10 year Treasury yield failed to meaningfully breakthrough 1.60%. But, if that happens today, look for stocks to drop in response, as rising yields remain the biggest headwind on stocks in the near term.

As for the reasons behind these drops, former Merrill Lynch trader Tom Essaye told Bloomberg that there was “a rollover in a lot of the momentum plays in the market — not just Bitcoin, but Tesla and tech stocks…” and the interest is coming out of these plays now. Click here to read the full article.

According to Tom Essaye of the Sevens Report, the core issue with bond yields has been economic growth. “Due to economic re-openings, stimulus, and vaccine optimism, global investors are pricing in a huge jump…” he wrote in a Thursday investor’s note. Click here to read the full article.

“While the S&P 500 may be facing structural headwinds due to tech weakness, much of the rest of the market…” Tom Essaye, founder of Sevens Research, said in his daily Sevens Report. Click here to read the full article.

“While the S&P 500 may be facing structural head-winds due to tech weakness, much of the rest of the market…” explained Tom Essaye, Sevens Report founder, in a note. Click here to read the full article.

“We’ve seen a rollover in a lot of the momentum plays in the market — not just Bitcoin, but Tesla…” Tom Essaye, a former Merrill Lynch trader who founded “The Sevens Report” newsletter, said by phone. Click here to read the full article.

“While the S&P 500 may be facing structural head-winds due to tech weakness, much of the rest of the market…” Tom Essaye, founder of Sevens Report, said in a note. Click here to read the full article.

What’s in Today’s Report:

U.S. equity futures are rallying with most global markets this morning as economic data mostly topped estimates overnight while there is a renewed sense of stimulus optimism as the $1.9T relief bill moves to the Senate today. President Biden also said that vaccine supplies will be sufficient to vaccinate all U.S. adults by the end of May, earlier than previously thought, which is offering further support to risk assets this morning.

Final Composite PMI data from February was largely upbeat with the Eurozone figure jumping to 48.8 vs. (E) 48.1, which helped offset a slight monthly dip in the Chinese headline.

Today is lining up to be a fairly busy day from a catalyst standpoint as there are two notable economic reports to watch: ADP Employment Report (E: 165K) and ISM Services Index (E: 58.7), both of which have the potential to move markets.

There are multiple Fed speakers to watch today: Harker (10:00 a.m. ET), Bostic (12:00 p.m. ET), Evans (1:00 p.m. ET), and Kaplan (6:05 p.m. ET), while markets will also be following any developments regarding the stimulus bill as it moves to the Senate today.

As long as economic data does not indicate a significant slowdown in the pace of the recovery, Fed speak remains very dovish, the legislative process with the stimulus bill remains smooth, and potentially most importantly, the bond market continues to trade in an orderly fashion, then stocks should be able to hold this week’s rebound. However if there are negative surprises regarding any of those market influences Monday’s sizeable gains could be given back in a hurry.