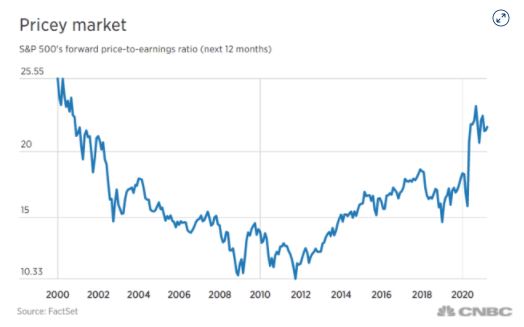

Market Multiple Table: April Update

What’s in Today’s Report:

- Market Multiple Table: April Update

Stock futures are modestly lower this morning following a quiet night of news as yesterday’s strong rally in U.S. equities is digested while international markets were mostly higher overnight.

Economically, China’s PMI Composite Index rose 1.4 points to 53.1 in March while the Eurozone Unemployment Rate edged up to 8.3% vs. (E) 8.1% in February, however neither report is materially moving markets this morning.

Today, there is just one economic report to watch: February JOLTS (E: 6.850M) and no Fed officials are scheduled to speak.

With limited catalysts on the calendar today, traders are most likely to be focused on coronavirus case trends and lockdown measures (both of which have been quietly on the rise lately) as well as bond markets.

Negative COVID headlines could result in some profit taking following yesterday’s big gains and any signs of another disorderly rise in bond yields given the firming economic growth expectations could also weigh on stocks, namely tech shares.