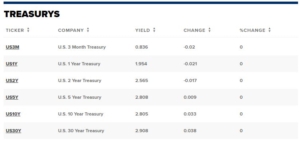

Yield Curve Update

What’s in Today’s Report:

- Yield Curve Update (Are Recession Risks Rising?)

- Why European Energy Companies Buying Gas in Rubles Matters to Stocks

- Q1 GDP – Not as Bad as It Looks

Futures are moderately lower following underwhelming earnings and guidance from AMZN and AAPL.

AMZN results underwhelmed the street (especially margins) while APPL beat earnings but had cautious guidance for Q2 based on supply chain issues.

Economically, inflation pressures remained high as core EU HICP (their CPI) rose 3.5% yoy vs. (E) 3.1%.

Today focus will be on inflation as we get two important readings: Core PCE Price Index (E: 0.3%, 5.3%) and the Employment Cost Index (E: 1.1%). Markets will want to see the actual numbers miss estimates, and in doing so further hint at a peak of inflation. If the opposite happens (the numbers are hotter than estimates) that will further pressure stocks. We also get Consumer Sentiment (E: 65.6) and the Inflation Expectations sub-index will be watched closely.

On the earnings front, some important results today include: XOM ( $2.25), CVX ($3.44), CL ($0.74).