What Will Move Bond Markets

For the past two weeks, we’ve told you via these free excerpts that the markets were entering a critical six-week period that ultimately would decide whether the rally in stocks continues… or reverses.

Well, that six-week stretch of events started with a bang last Friday as Fed Vice Chair Fischer surprised markets by basically saying Friday’s jobs report would decide whether the Fed would hike rates in September.

As a result, bond yields spiked and stocks dropped.

And, if Friday was any indication, we’re in for a wild ride as the markets navigate the remaining 6 key critical central bank/macro events between now and September 26th (more on that below).

We never like to see the markets go down as all of us are generally “long” stocks, but Friday was a good day for us here at The Sevens Report, because it validated what we’ve been saying to our paid subscribers for the past several weeks:

Specifically, that whether stocks resume the July rally or break down from here will depend on the bond market, and as a rule, anything that sends bond yields up will be negative for stocks, and anything that sends bond yields down will be positive for stocks.

While other research publications were simply providing recaps of a dull market during the majority of August, we were consistently telling our subscribers that the bond market is the key and the coming several weeks were going to be critical—and on Friday afternoon (and continuing today), our advisor subscribers were able to demonstrate to their clients they were on top of markets and in control of their portfolios!

In fact, one subscriber wrote in and said it was the “Plain English” analysis of the bond market that’s helped him strengthen a relationship with a high net worth client, and he’s pretty sure that he’s going to get an additional allocation because, as the client said, his other advisors seemed to have “taken August off” given the quiet market.

That’s the kind of feedback that makes the early wake ups and long hours of work worth it, and the best part is that our subscriber only had to spend less than 10 minutes each morning reading our daily macro report. That’s how The Sevens Report

helps advisors grow their business.

Every trading day at 7 a.m. we provide plain English, concise analysis of:

-

Stocks

-

Bonds

-

Commodities

-

Currencies and

-

Economic Data

And, our daily report takes less than 10 minutes to read each day!

Finally, we do it at a cost that’s substantially less than our competition (and less than one client lunch per month), and that’s why we continue to believe we offer the best value in the paid research space!

Given last Friday’s “hawkish” surprise from Fed Vice Chair Fischer, it’s critically important for all advisors to understand what is really driving the bond market

(it’s not a Fed rate hike) because where bonds go from here will determine the next move in stocks.

We’ve included an excerpt of that research as a courtesy.

Understanding What Will Move the Bond Markets (It’s Not Rate Hikes)

The question of when the Fed hikes rates has come back to the forefront for investors, as expectations for a rate hike in September or December have increased following the hawkish comments from last Friday.

But it is very important to understand that while the media will focus on the Fed hike drama, easily the most important thing to understand about the bond market right now is that the Fed has little to no control over whether 10- and 30-year Treasury yields stay in a downtrend (good for stocks), or reverse and start to trend higher (bad for stocks).

Whether the Fed hikes in September, December or 2017 won’t resolve the major issue facing stocks right now, which is the near-term direction of global 10- and 30-year bond yields.

Instead, there are two other central banks that control the direction longer-dated Treasury yields:

-

The European Central Bank (ECB) and

-

The Bank of Japan (BOJ)

For US stock and bond investors, what those banks do in September is much, much more important than what the Fed does between now and December.

Now, I said that the Fed doesn’t control longer-term interest rates anymore to a friend this weekend, and he was incensed that I could utter anything so “stupid.”

But, I pointed out that over the past two years, we’ve seen the Fed:

-

End the QE program and

-

Hike Fed funds 25 basis points

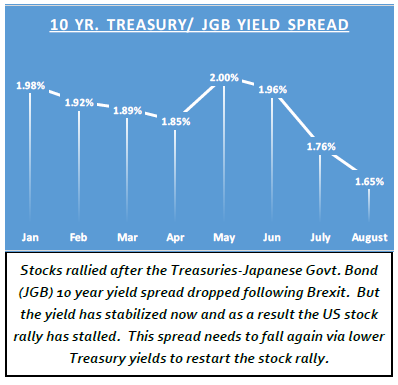

Yet, during that two-year period, yields on the 30-year Treasury are down 80 basis points, from 3.1% in December 2014 to 2.1% post Brexit, and yields on the 10-year Treasury are also down 100 basis points (or 1%), from 2.3% to 1.33% post Brexit.

CHART

So my question to him was: If the Fed is still in control of longer-term Treasury yields, how can this be possible?

The answer is they aren’t in control any longer as the Treasury market has been overrun by foreign buyers due to the actions of the BOJ, ECB and now BOE.

The reason this is important for advisors and their clients is this:

Between now and year end, whether stocks resume their rally will depend on whether the ECB and BOJ are more hawkish than expectations, not the Fed.

If that happens, yields on Bunds and JGBs (Japanese Government Bonds) will rise and that will cause Treasury yields to rise too, regardless of whether Yellen trots out with a dove on her shoulder and promises to never hike rates again!

The critical bottom line is this: The financial media will be totally consumed with whether the Fed is going to hike rates in September, but from a stock standpoint (specifically whether stocks rally in Q4 or pullback) what the ECB does on September 8th and what the BOJ does on September 21st are much, much more important.

They are in control of longer-dated Treasury yields, and longer-dated Treasury yields will decide the next move in stocks and we will make sure you stay focused on what’s really important in the bond markets over the coming six weeks.

Make Sure You Have the Plain English and Actionable Analysis to Navigate the Next Six Weeks

We will give our advisor and investor subscribers the plain English talking points to help them turn any Fed or central bank-based volatility into an opportunity to demonstrate their knowledge of markets and impress current clients and prospects.

And, we are going to provide that same level of analysis for the remaining 6 key events that are coming in September, events that will decide whether this rally extends into the fourth quarter

- Friday’s Jobs Report: Will the number increase the odds of a September rate hike (and if so cause more short term declines in stocks).

- The ECB Meeting September 8th: Will the ECB hint at more stimulus (bullish) or not (bearish)?

- The Fed Meeting September 21st: Will the Fed hike rates (very bearish), hint at hiking rates in December (bearish) or stay ultra-dovish (bullish)?

- The Bank of Japan Meeting September 21st: Will the BOJ adopt “Helicopter Money Light” (bullish), or just do another inconsequential easing like in July (bearish).

- First Presidential Debate September 26th: Will Trump get back into the race (bearish short term – and this is not a political opinion) or will Clinton maintain a comfortable lead (not bearish).

- International Energy Forum September 26th: Will OPEC and Non-OPEC members agree on a global production but (bullish oil) or not (very bearish oil).

If all we do is help you navigate the month of September correctly and help you get properly positioned in client accounts for the fourth quarter, we will have more than covered our subscription costs.

If you do not have a morning report that is going to give you the plain spoken, practical analysis that will help you navigate the coming six weeks, then please consider a quarterly subscription to

The Sevens Report.

There is no penalty to cancel, no long-term commitment, and it costs less per month than one client lunch!

With thousands of advisor subscribers from virtually every firm on Wall Street and a 90% initial retention rate, we are very confident we offer the best value in the private research market.

I am continuing to extend a special offer to new subscribers of our full, daily report that we call our “2-week grace period.”

If you subscribe to The Sevens Report today, and after the first two weeks you are not completely satisfied, we will refund your first quarterly payment, in full, no questions asked.

Click this link to begin your quarterly subscription today.

Value Add Research That Can Help You Grow Your Business in 2016

Our subscribers have told us how our focus on medium-term, tactical opportunities and risks has helped them outperform for clients and grow their businesses.

We continue to get strong feedback that our report is: Providing value, helping our clients outperform markets, and helping them build their books:

“Thanks for your continued insight; it has saved my clients over $2M USD this year… Keep up the great work!” – Top Producing FA from a National Brokerage Firm.

“Let me know if there is anything else that you need from us. Thanks again for everything. I really enjoy the Report – it is helping me grow my business and stay on top of things.” – Independent FA.

“Great service from a great company!!” – FA from a National Brokerage Firm.

“Great report. You’ve become invaluable to me, thanks for everything…! – FA from a Boutique Investment Management Firm.

Subscriptions start at just $65 per month, billed quarterly, and with the option to cancel any time prior to the beginning of the next quarter, there’s simply no reason why you shouldn’t subscribe to The Sevens Report right now.

Begin your subscription to The Sevens Report right now by clicking this link and being redirected to our secure order form.

Finally, everything in business is a trade-off between capital and returns.

So, if you commit to an annual subscription, you get one month free, a savings of $65. To sign up for an annual subscription simply click here.

Best,

Tom

Tom Essaye

Editor, The Sevens Report