Why Rising Treasury Yields Are a Headwind on Stocks

What’s in Today’s Report:

- What is Country Garden and Why Does It Matter?

- Equity Risk Premium: Why Rising Bond Yields Are a Headwind on Stocks

- Chart – Growth Stocks Approach Key 2023 Support

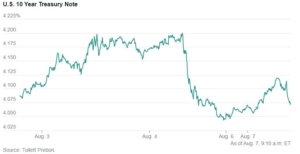

U.S. equity futures are tracking global markets lower this morning amid more negative news flow out of China while Treasury yields continue to test to cycle highs with the 10-Year Note yield above 4.20%.

Multiple Chinese economic reports badly missed estimates overnight with Retail Sales notably rising just 2.5% vs. (E) 4.2% in July.

The bad data and renewed concerns about the property market prompted surprise rate cuts by the PBOC but the policy action was seen as underwhelming by investors and markets traded with a decisive risk-off tone overnight.

Looking into today’s session, the headlines out of China will continue to influence money flows, however there are several key U.S. economic reports to watch this morning including: Retail Sales (E: 0.4%), Empire State Manufacturing Index (E: -0.4), Import & Export Price (E: 0.2%, 0.1%), and the Housing Market Index (E: 56).

Markets continue to look for “Goldilocks” dynamics in the data, consistent with easing growth, a loosening labor market, and continued drop in inflation. Anything that contradicts those trends could further risk assets including stocks today.

There is also one Fed speaker today: Kashkari (11:00 a.m. ET) but it is doubtful he wavers from the Fed’s narrative and is unlikely to move markets.