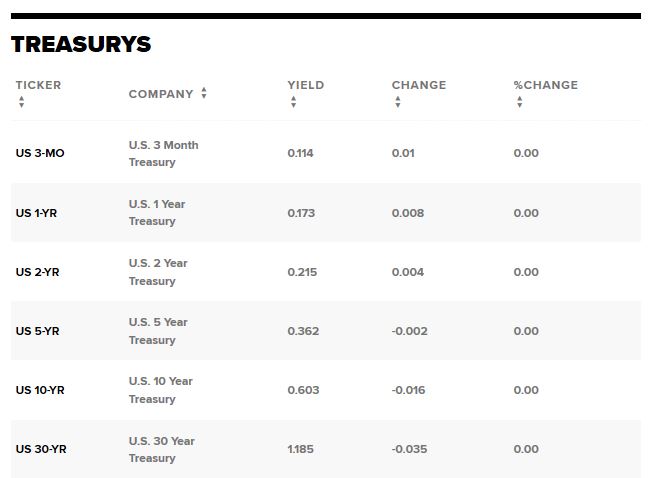

The initial market reaction to the CPI release was a hawkish one

Oil prices decline to session lows: Sevens Report Co-Editor, Tyler Richey, Quoted in MarketWatch

Oil futures move up after CPI data, OPEC’s latest forecast for growth in oil demand

The initial market reaction to the CPI release was “a hawkish one, which saw oil prices decline to session lows,” said Tyler Richey, co-editor at Sevens Report Research. “Hawkish central bank policy is bad for the oil market because high interest rates over time act as a steady headwind on global growth and ultimately that weighs on consumer demand expectations.”

Looking at the reaction in the rates markets, “hawkish money flows were only modest, and investors are still pricing in a June rate cut from the Fed, just with a slight dip in confidence,” Richey said.

Also, click here to view the full MarketWatch article published on March 12th, 2024. However, to see the Sevens Report’s full comments on the current market environment sign up here.

If you want research that comes with no long term commitment, yet provides independent, value added, plain English analysis of complex macro topics, then begin your Sevens Report subscription today by clicking here.

To strengthen your market knowledge take a free trial of The Sevens Report.