10-Year Treasury Yield Dips to 4.1% After ADP Miss

Soft jobs data reignited slowdown concerns, keeping the 10-year yield locked in its 2025 trading range.

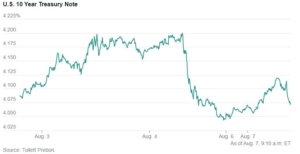

TNX: My Technical Take on 10-Year Treasury Yields

Treasury yields eased moderately following this week’s weaker-than-expected ADP jobs report. The 10-year Treasury Note yield (^TNX) slipped five basis points to 4.1% on Wednesday, extending its pattern of tight range trading that has persisted through most of 2025. Tom Essaye, president of Sevens Report, noted that the 10-year yield remains technically neutral until a new extreme is reached. He added that the decline was driven more by growth and inflation expectations than Fed policy, as the benchmark yield tends to track economic momentum rather than short-term rate decisions. If the upcoming government jobs report echoes ADP’s weakness, Essaye cautioned that renewed slowdown fears could push investors back toward the safety of long-dated Treasuries—“just as they always do, despite fiscal concerns.”

Also, click here to view the full article on Moneyshow.com published on October 3rd, 2025. However, to see the Sevens Report’s full comments on the current market environment sign up here.

If you want research that comes with no long term commitment, yet provides independent, value added, plain English analysis of complex macro topics, then begin your Sevens Report subscription today by clicking here.

To strengthen your market knowledge take a free trial of The Sevens Report.

Join hundreds of advisors from huge brokerage firms like Morgan Stanley, Merrill Lynch, Wells Fargo Advisors, Raymond James, and more! To start your quarterly subscription and see how The Sevens Report can help you grow your business, click here.