What’s in Today’s Report:

- Market Multiple Table – August Update

- Oil Tests 2023 Highs – Chart

U.S. futures are modestly higher as deflationary Chinese price data is being offset by risk-on money flows in Europe fueled by a rebound in bank stocks.

The Italian government clarified that a windfall tax on bank profits would be capped, sparking a relief rally in European financials and general risk-on trade in global markets.

Economically, Chinese CPI fell -0.3% vs. (E) -0.5% and PPI fell -4.4% vs. (E) -4.0% revealing the emergence of deflationary price trends as the world’s second largest economy struggles to generate any meaningful growth momentum.

There are no notable economic reports and no Fed officials are scheduled to speak today which is setting the session up to be fairly quiet as traders await tomorrow’s CPI release.

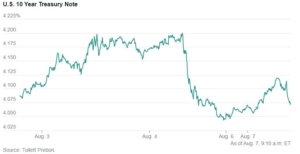

There is a 10-Yr Treasury Note auction at 1:00 p.m. ET, however, and after yesterday’s strong 3-Yr Note auction, bond investors will be looking to see solid demand for longer duration Treasuries given the recent rise in yields, otherwise a further rise in longer-term rates will likely weigh on stocks (especially high valuation corners of the market).

Finally, earnings season is winding down but we will hear from DIS ($0.99) and WYNN ($$0.59) after the close and their quarterly results could shed some new light on the health of the consumer.