CPI Preview: Good, Bad, and Ugly

CPI Preview: Good, Bad, and Ugly – Start a free trial of The Sevens Report.

What’s in Today’s Report:

- CPI Preview: Good, Bad, & Ugly

- “Soft Components” of the NFIB Small Business Optimism Index Fall to GFC Lows

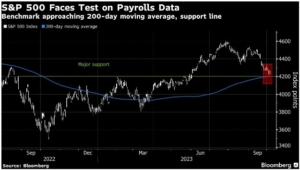

- Chart – Equal-Weighted S&P 500 Index (RSP) Remains in Steep Downtrend, Underscoring Thin Market Breadth

U.S. equity futures are modestly higher this morning despite escalating tensions in the Middle East overnight as investors embrace a continued pullback in global bond yields after steady inflation data in the EU overnight.

Economically, German CPI was unchanged from August, coming in at 4.5% y/y in September, meeting estimates. The inline inflation print is helping bonds continue to stabilize and supporting modest risk-on money flows this morning.

Today, focus will be on economic data early with PPI (E: 0.3% m/m. 1.2% y/y) and Core PPI (E: 0.2% m/m, 2.1% y/y) due out ahead of the bell.

From there focus will turn to the Fed with multiple officials scheduled to speak: Waller, Bostic, Collins. Additionally, the latest FOMC meeting minutes will come at 2:00 p.m. ET.

Bottom line, if PPI is more or less inline with estimates and the FOMC minutes and Fed chatter over the course of the day continue to support the less-hawkish narrative of recent. Then this week’s rally can continue, however and reversal back higher in yields will pressure stocks and other risk assets.

Join hundreds of advisors from huge brokerage firms like Morgan Stanley, Merrill Lynch, Wells Fargo Advisors, Raymond James, and more! To start your quarterly subscription and see how The Sevens Report can help you grow your business, click here.