Sevens Report 7.16.14

Equities

Market Recap

Markets declined Tuesday as cautious comments from Fed Chair Yellen offset strong economic data, although stocks managed to close well off the worst levels of the day. The S&P 500 fell -0.2%.

Tuesday initially started pretty well as futures were higher after several major companies beat earnings (GS, JNJ, CMA, JBHT, JPM) and economic data (June retail sales, July Empire State manufacturing) beat estimates. The Dow Industrials hit a new all-time high, and the S&P 500 inched closer to its recent high, but markets reversed on the Yellen appearance before Congress.

I’ll cover it more in depth below, but Yellen’s comments caused the small caps and “momentum” sectors (biotechs and Internet stocks) to come for sale hard (you’ll see why in a minute), and that dragged down the entire market.

But, as has generally been the case since last Thursday, there was no real conviction or follow-through to the selling Tuesday. The S&P 500 bottomed down -0.5% shortly after midday, and then began a slow rally back toward flat before selling off slightly into the close.

Bottom Line

The market has been consolidating since the highs of July 7, and that continued yesterday.

The price action in small caps and momentum names is disconcerting, but most of the selling that’s going on in those sectors is by fast-money funds and algos, not real money materially reducing exposure (like we saw in April). Europe has also been weak and likewise needs to be watched, but the fundamentals behind the market remain broadly positive.

All that said, I don’t think this period of consolidation is over just yet, and it wouldn’t shock me if we have another “scare” to the downside on some sort of negative news over the coming days.

Earnings are helping to support markets (although it’s still early), but I’d continue to like to see the SX7P (European banking index) bottom before buying back into Europe, and for the NBI and QNET (biotechs and Internet indices) hold the lows of last week before allocating anything further into SPHB and more-cyclical sectors.

Again, this looks like a normal consolidation to me (rather than a correction), but I don’t think it’s over just yet.

Yellen’s Testimony Wasn’t ‘Hawkish,’ But It Did Cause Stocks to Decline.

The general consensus of Fed Chair Yellen’s statement and Q&A in front of the Senate yesterday was that she was incrementally “hawkish.” But that wasn’t really the case.

The main sentence that was being spun as “hawkish” was her commentary that “if the labor market continues to improve more quickly than anticipated by the Committee … then increases in the Federal Funds rate target would occur sooner and be more rapid than currently envisioned.”

Translation: If the jobs market improves and inflation accelerates, we’ll pull forward when we raise rates and how quickly we raise them.

That’s not a hawkish statement – it’s common sense.

The reason the market traded down yesterday was thanks to a totally separate piece of information – the Fed’s semi-annual report to Congress. It contained the statement that “valuation metrics in some sectors do appear substantially stretched – particularly those for smaller firms in the social media and biotechnology industries. … Moreover, implied volatility for the overall S&P 500 index, as calculated from option prices, has declined in recent months to low levels last recorded in the mid-1990s and mid-2000s, reflecting improved market sentiment and, perhaps, the influence of ‘reach for yield’ behavior by some investors.”

So, the Fed singled out bio-tech and social media as overvalued, and that statement echoes recent comments Yellen has made about pockets of “froth” in the equity markets. Importantly, though, she described the valuation of the broader stock market as “not far above historical averages,” so this was more about addressing the overvaluation in “momentum” sectors more than it was declaring the stock market “irrationally exuberant.”

The Fed signaling out “momentum sectors” is a unexpected headwind (the fear is a repeat of April where a sharp decline in those sectors drags the entire market lower).

But, and that’s not exactly new messaging, and more importantly, the bottom line is that the outlook for the Fed did not change in yesterday’s testimony (and likely won’t change today, either).

Economics

Both economic releases yesterday beat estimates and painted an encouraging picture for consumer spending and economic activity in July. But, neither resulted in an equity-market rally, as comments by Fed Chair Yellen overshadowed the hard data.

Retail Sales

- June Retail Sales rose 0.2% vs. (E) 0.6%.

Takeaway

June retail sales disappointed on the headline yesterday morning, but that was a bit misleading. The details of the report were good and there were positive revisions to April (0.5% from 0.2%) and May (0.2% from 0.0%). The “control” number — which is retail sales ex-autos, building materials, and gasoline stations — rose +0.6% in June, the 4th month in a row.

Bottom line, the disappointing headline of yesterday’s retail sales report for June was misleading and the report was actually pretty good. And, while not reflecting robust consumer spending, the strong June “control” figure and positive revisions will help ease some of the general concern regarding consumer spending. This report was a positive for the economy.

Empire State Manufacturing Survey

- General Business Conditions Index rose to 25.60 vs. (E) 17.80 in July.

Takeaway

Manufacturing activity accelerated to a 4-year high in the greater New York area in July. Both the headline and details of the report were good, as new orders (the leading indicator within the report) were little-changed but remain strong at 18.77.

Empire State manufacturing hasn’t been a very good predictor of the broader national manufacturing PMIs in 2014. Regardless, it’s encouraging for the market to see growth in the manufacturing sector continuing in July, especially in the context of constant worries about the strength of the manufacturing recovery.

Focus will now turn to the Philly Fed manufacturing index Thursday. But the bottom line is this first data point from July implies the recovery in the manufacturing sector is accelerating further and that’s anecdotally encouraging for the economy as a whole.

Commodities

Commodities were almost universally lower yesterday, in part thanks to a stronger dollar (+0.3%). The sole exception was copper, which was only slightly higher on better than expected Chinese economic data. The benchmark commodity tracking index ETF, DBC, fell to a 5-month low before bouncing slightly into the close.

Precious metals got hit again yesterday. Gold fell -0.8% while silver gave up a more-modest -0.4%. Nearly all of the session losses in gold came in the first 15 minutes of Yellen’s testimony (when her statement was released and then feverishly dissected by the news-reading algorithms). Gold smashed through support in that $1300—$1310 range in heavy selling before finding support in the $1290 region.

Gold futures were able to hold the 50-day moving average at $1,292.40. But the reason it was defended was more a result of shorts taking profits rather than new longs initiating positions. Bottom line, it appears that the broken uptrend line was more important over the near term than initially expected. Despite the 3 other supporting factors in the market (the bullish cross in the moving averages, the rising number of net longs, and the underlying inflation bid), the bears still have the momentum and we could see a further dip or at the very least some further consolidation here below $1,300.

Elsewhere in metals, copper was the only commodity to finish higher yesterday, adding a very modest +0.05% thanks to some better than expected economic data. A Chinese report showed that lending increased at a higher than expected rate last month, which helped reverse losses ahead of the release.

Going forward, prices remain somewhat extended as the recent rally from $3.00 was a sharp one; therefore we’d like to see a further pullback to around $3.20 before the risk/reward would be favorable to initiate long positions in copper. But, looking ahead, the improvement in the global economy will continue to be a tailwind on copper prices as a result of higher demand.

Crude oil futures resumed their downtrend Tuesday after seeing a bounce on Monday. WTI fell -1.01% yesterday but importantly held support at the 200-day moving average ($99.81). But, WTI still has some significant downside momentum and until we see a break of the sharp downtrend that has been in place since the mid-June highs, we will remain sidelined. Such a break would require a close above $101.25.

Fundamentally, today is inventory day for crude oil and the products, and a bullish report may facilitate a short-covering rally and a close above the aforementioned technical level. Expectations are: -2.6M bbls in WTI Crude, 700k bbls increase in RBOB Gasoline, and + 2M in distillates.

Natural gas traders retested trend support at the $4.10 level yesterday as futures fell -1.3%. Like crude oil, natural gas also remains a “falling knife” here. Even though the risk/reward setup for initiating a long here is favorable, like in WTI crude there is significant downside momentum in the very short term, and we would like to see a close above the steep downtrend line (above $4.15 or so) before initiating a long position.

Currencies & Bonds

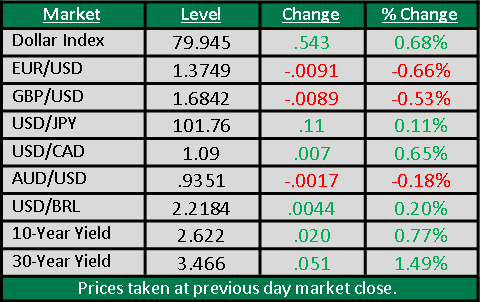

The dollar was nearly universally stronger yesterday courtesy of the good economic data (retail sales and Empire State manufacturing survey) and a “hawkish” take on Yellen’s testimony. The Dollar Index rose +0.27%.

The only major currency that ended the day higher vs. the dollar was the British pound, as it rose +0.39% to (just off a new 6 year high) after Great Britain June CPI rose to 1.9% year-over-year, much higher than the 1.6% consensus.

The headline jump in inflation year over year was a bit eye-popping, but it’ll probably prove temporary. That’s because the spike higher was caused by price increases for footwear and apparel. But, the increase will likely be temporary because of seasonal adjustments. Normally, retailers in Great Britain heavily discount summer clothing in June, so the seasonality anticipates this discount. This year, though, the retailers appear to have not as aggressively discounted in June, and will likely spread out discounts over the summer months. So, that should result in some seasonality “payback” in the form of price declines in July/August.

Regardless, clearly inflation is trending higher in the UK, as is economic growth. This is just reinforcing the point that the Bank of England will be the first major central bank to raise interest rates, perhaps as early as this year. The pound remains the single-most-attractive currency vs. the dollar right now.

Staying in Europe, the euro was almost the worst performer vs. the dollar yesterday, falling -0.38%, on a combination of factors: dollar strength, a German ZEW Business Expectations Index miss, and “dovish” comments by ECB President Mario Draghi (he said a strong euro is a threat to growth and that asset purchases (QE) are well within the scope of the ECB). None of the comments were new, but Draghi wanted to try to talk the euro down and appears to have been moderately successful (the euro is down again this morning and through support at 1.355).

Keep in mind, a weakening euro is what the “Europe bulls” want right now, so a declining euro is a needed tailwind for European shares, if it continues.

Looking at the commodity currencies, the Loonie was the worst performer vs. the dollar yesterday, falling -0.4% ahead of a manufacturing report earlier today. The Loonie is now sitting on key support at $0.9260, and if that’s broken, look for the declines to accelerate. The Aussie was also slightly lower vs. the dollar after the Reserve Bank of Australia’s June meeting minutes were taken as slightly “dovish” in tone. (Nothing shocking was said; just general mention of concern about the economy.) But, the Aussie remains in the middle of the trading range ($0.92-$0.94).

Turning to bonds, the 30-year traded in a big range yesterday. It initially traded down nearly -0.3% on the strong economic data and Yellen comments, but then rebounded and rallied nearly +0.3% later on in the testimony, before giving back those gains to finish basically unchanged. Meanwhile the yield on the 10-year was also unchanged.

Treasuries remain buoyant but seem a touch confused at the moment, as the market tries to “game” the Fed’s potential normalization strategy within the context of foreign demand for Treasuries, an accelerating economy and bottoming inflation. And, in the near term, money flows from the two aforementioned sources are trumping the fundamentals of the two latter sources. Bottom line is that Treasuries remain above the uptrend of 2014. Until they decisively break that downtrend, then the short-term benefit of the doubt remains with the bulls, despite growing fundamentals that suggest Treasuries should be declining.

Have a good day,

Tom