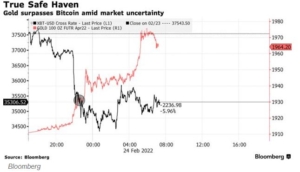

Tom Essaye Quoted in Bloomberg on February 24, 2022

Bitcoin’s Digital Gold Luster Fades as Customary Havens Win Out

Gold is doing exactly what it should be doing right now, but it’s a much more mature asset and it’s got a proven history in these types of conflicts of how it trades…said Tom Essaye. Click here to read the full article.