Sevens Report’s Tom Essaye appeared in Yahoo Finance on November 23, 2018

Sevens Report’s Tom Essaye appeared in Yahoo Finance on November 23, 2018. His take on oil, market volatility, stocks and more. Watch the entire clip here.

Sevens Report’s Tom Essaye appeared in Yahoo Finance on November 23, 2018. His take on oil, market volatility, stocks and more. Watch the entire clip here.

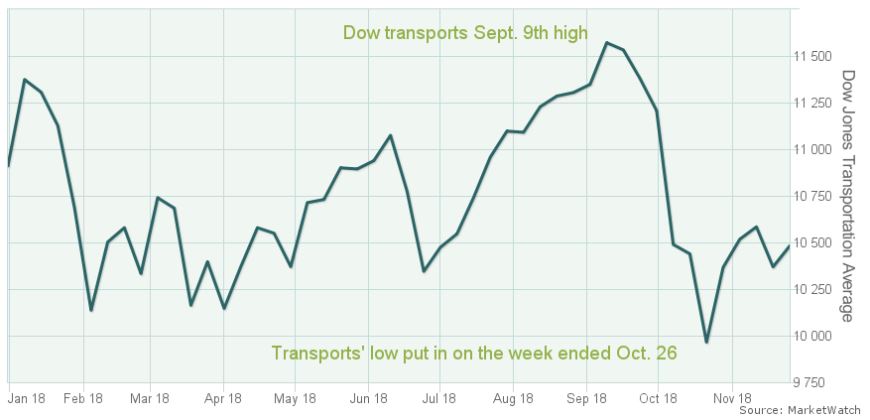

Sevens Report’s Co-editor Tyler Richey quoted in MarketWatch on November 26, 2018. His take on Dow Theory. Read the full article here.

What’s in Today’s Report:

Futures are trading slightly lower this morning on an uptick in trade war fears following an otherwise quiet night.

After the close yesterday, the WSJ ran an interview with Trump where he said he was ready to move forward with increasing tariff rates (from 10% to 25%) in early 2019 and delaying the hike per China’s request was “highly unlikely.”

Today, there are a few potential catalysts on the schedule. Economically, there are three reports due out: S&P CoreLogic Case-Shiller HPI (E: 0.3%), FHFA HPI (E: 0.3%) and Consumer Confidence (E: 136.5).

Meanwhile on the Fed front, Clarida speaks ahead of the open (7:45 a.m. ET) while Bostic, George, and Evans speak on a panel in NY this afternoon (2:30 p.m. ET).

With Powell’s speech later this week still a major focus of the market, the Fed chatter will be watched closely while the market will remain very sensitive to any further rhetoric on the trade front (the other big event being the G20) after Trump’s comments yesterday afternoon.

What’s in Today’s Report:

Futures are surging and global markets are up 1% thanks to apparent progress on the EU/Italy budget standoff.

Italian deputy PM Salvini said over the weekend that Italy wasn’t “stuck” on the 2.4% budget deficit, adding to the momentum that a compromise might be achieved.

Economic reports overnight were again disappointing. Japanese flash manufacturing PMI missed estimates (51.8 vs. (E) 53.0), as did German IFO business expectation (98.7 vs. (E) 99.2.

There are no notable economic reports or Fed speakers today, so focus will remain on the tech sector. Tech traded with some decent relative strength Friday, and if it can build on that today, then we could see a good bounce back rally. Conversely, if tech fails to rally, then so too will the boarder markets.

What’s in Today’s Report:

Futures are marginally lower as markets digest recent volatility following a mostly quiet Thanksgiving holiday.

Regarding U.S./China trade, there were numerous articles published overnight on the upcoming summit and while they varied in tone (both positive and negative) none of them changed expectations for the event.

Economically, the Nov. EU flash composite PMI declined and missed expectations, falling to 52.4 vs. (E) 53.0. That soft reading, combined with new lows in oil (down 2%) are the two “reasons” for the decline in futures this morning.

Today will be a typically quiet post-Thanksgiving Friday but there is an important economic report to watch: Composite Flash PMI (E: 54.8). Economic data has been more mixed lately, and a soft number here will fuel concerns the U.S. economy is losing momentum.

Finally, keep in mind that U.S. equity markets close at 1:00 p.m. ET.

Sevens Report’s Tom Essaye appeared on Bloomberg Radio on November 19, 2018. Listen to the full audio clip here.

Sevens Report’s Tom Essaye quoted in Nasdaq on November 20, 2018. Read the full article here.

What’s in Today’s Report:

Futures are enjoying a modest oversold bounce following a generally quiet night.

Italy will be in focus today as the European Commission will issue a decision on the resubmitted budget and rejection is likely. Positively, however, there were some reports Italy would be open to negotiation on the proposed budget, and that helped fuel the bounce this morning.

There were no notable economic reports overnight.

Today should be a generally quiet day as travel picks up for the Thanksgiving holiday. But, that said, there are three notable economic reports this morning: Durable Goods (E: -2.5%), Jobless Claims (E: 215k), Existing Home Sales (E: 5.21M). Bottom line, tech remains key in the short term. If Nasdaq and FDN can bounce, stocks can recoup some of the week’s losses.

Everyone please have a happy and safe Thanksgiving!