What’s in Today’s Report:

- A Game of Multiples

- Why the ECB Decision Is the Most Important Event this Week

S&P futures are climbing this morning, tracking gains in overseas markets as investors digest positive trade war headlines from Monday and better-than-feared earnings to kick off a very busy week of the Q2 reporting season.

There were no notable economic reports overnight and macro news was limited.

Looking into today’s session, focus will be on the micro as earnings season picks up however there are two economic data points on the housing market: FHFA House Price Index (E: 0.3%) and Existing Home Sales (E: 5.340M). Meanwhile there are no Fed officials scheduled to speak.

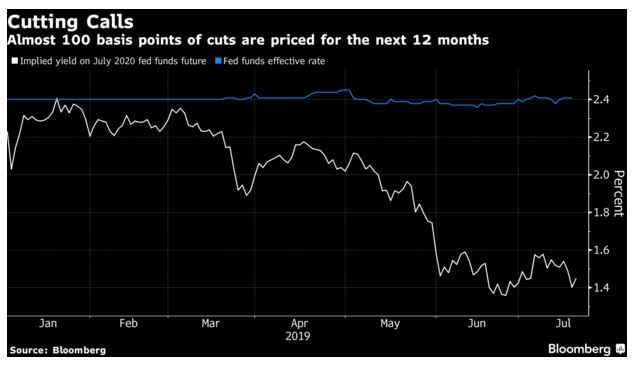

In the bond market, there is a 2-Year T-Note Auction today at 1:00 p.m. ET which could affect the yield curve. If we see the curve flatten further as it did last week, that could weigh on stocks again but contrarily, if we see the 10s-2s widen back out towards 30 basis points, that should support stocks broadly.

Earnings remain in the spotlight this week with notable reports coming from: KO ($0.62), LMT ($4.74), BIIB ($7.58), UTX ($2.04), JBLU ($0.57), and TRV ($2.32) ahead of the bell, while SNAP (-$0.10) and V ($1.33) will report after the close.