Fed Meeting Preview

What’s in Today’s Report:

- FOMC Preview

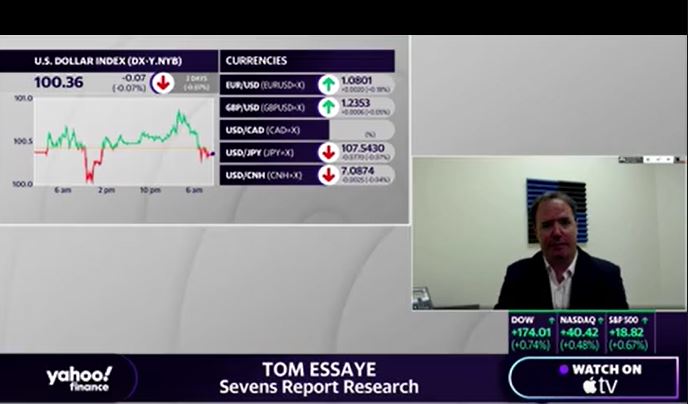

S&P futures are up 1% this morning, tracking European shares higher as economies around the globe begin to reopen while investor focus shifts ahead to the slew of earnings releases in the coming days as well as multiple central bank meetings this week.

Coronavirus headlines were mostly positive overnight as there were reports of expanded testing capabilities in the U.S., the growth rate of new cases continues to slow in the U.S., and states across the country are beginning the process of lifting COVID-19 containment policies.

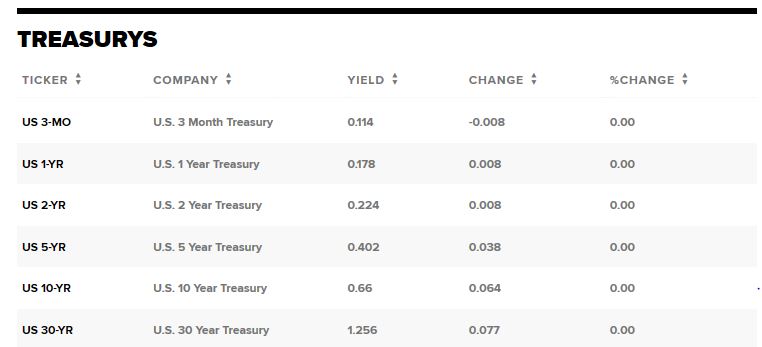

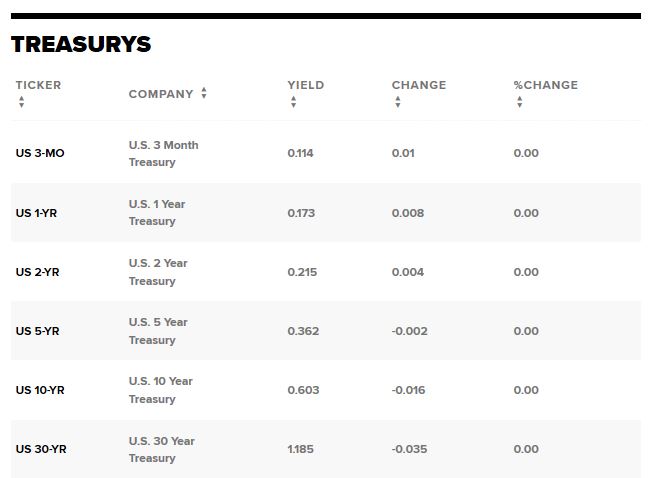

The FOMC meeting begins today (concluding tomorrow) while there are a few notable economic reports to watch this morning: International Trade in Goods (E: -%51.5B), S&P CoreLogic Case-Shiller HPI (E: 0.4%), and Consumer Confidence (E: 95.0).

Investors will be increasingly focused on earnings this week as we approach the peak of the Q1 reporting season.

There are several major corporations, from manufacturing to tech sectors, releasing results today including: MMM ($2.02), PEP ($ 1.02), PFE ($0.71), UPS ($1.23), CAT ($1.77), MRK ($1.39), LUV (-$0.48), BP ($0.28), AMD ($0.18), GOOGL ($10.97), F (-$0.10), CHRW ($0.71).