A Stimulus Driven Rebound for Brick and Mortar Retail?

What’s in Today’s Report:

- A Stimulus Driven Rebound for Brick and Mortar Retail?

- EIA and Oil Update

Futures are moderately higher on general optimism for several upcoming events. There was no notable news overnight to cause the rally in futures, however.

Politically, Biden is expected to sign the stimulus bill on Friday and now the focus is on infrastructure and trade.

On trade, Nasdaq futures are sharply higher on the potential for a U.S./China semiconductor trade group (which would potentially ease semiconductor supply issues) and on general optimism ahead of the U.S./China meetings in Alaska this weekend (relaxing of trade tensions is a potential additional tailwind on stocks, especially tech and industrials).

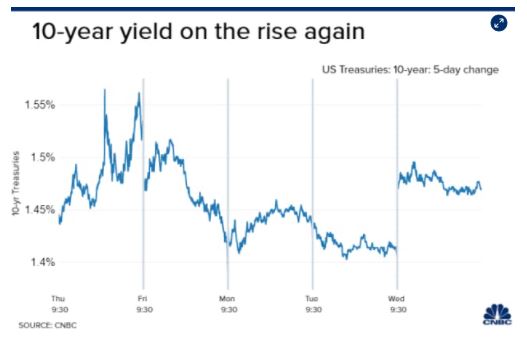

Today the focus will remain on rates and that makes the ECB Rate Decision (E: No Change) the most important event today. Markets fully expect ECB President Lagarde to say something specific or actually do something to show the ECB will not allow rates to rise too quickly. If that does happen look for the 10 year Treasury yield to fall further below 1.50% and for stocks to extend the rally. But, if Lagarde disappoints markets, expect rates to rise in response, and stocks to decline.

Other notable events today include Jobless Claims (E: 725K), 30-Yr Treasury Bond Auction at 1:00 p.m. and if both are solid, they will help support the rally.