What the ECB Balance Sheet Means for Stocks and Bonds

The Key to Europe—the ECB Balance Sheet (What It Means for Stocks and Bonds)

What Happened: Part of the reason we’ve seen a rally over the past two days in the Treasury market is because of Europe—specifically the “dud” of the first TLTROs late last week.

Not only was demand for the initial offering poor (86.4 billion vs. (E) 150 billion euros), but on Friday European banks actually repaid nearly 19 billion euros worth of the previous LTRO, making the total addition to the ECB balance sheet only about 67 billion (86.4B – 19B)—less than half of the 150 billion the market expected.

Why It’s Important: The size of the ECB balance sheet is very critical to the economic recovery in Europe. QE, TLTROs, ABS purchases and all the other acronyms are simply tools being deployed to accomplish the same goal—to get the ECB balance sheet to rise.

The logic goes that if the ECB can expand its balance sheet and pump money into the system, then they should create economic growth. That would in turn create inflation, which would then solve the deflation problem they are currently experiencing. (That script has “worked” in the US, UK and lately, Japan).

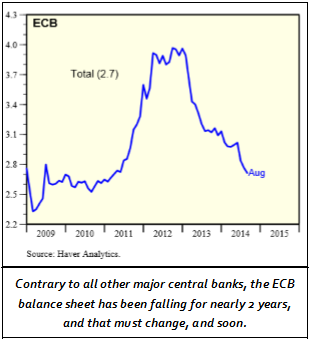

So, to keep things simple, an expanding balance sheet is inflationary and positive for growth, while a contracting balance sheet is deflationary. And as you can see from the chart, the ECB is the only major central bank whose balance sheet has been contracting.

How We Make Money Off It: If the ECB fails to materially expand its balance sheet, then deflation will get a tighter grip on the economy. European bonds will rally like they did for most of this year, and that will put upward pressure on Treasuries—just like it did from March to September.

As the ECB implements these measures (TLTRO, ABS), you will see the market waver in the short term between thinking the measures are working (and the balance sheet expanding, which is Treasury-bearish) and the measures failing (as in the case of last week, which is Treasury-bullish).

Treasuries will be much more sensitive to the short-term data from Europe than stocks. But importantly, as long as the ECB remains committed to expanding the balance sheet, any short-term rally is “noise” compared to the overall negative trend in bonds.

European stocks should be much less sensitive to short-term fluctuations than bonds. That’s because, as was the case last week, the failure of the initial TLTRO was just seen as further increasing the odds of QE. The ECB simply cannot fail to increase its balance sheet and spur a recovery—because if they do, it’s very likely the EU would split apart. (Southern European countries are not going to stay in the EU if deflation takes hold—they will break away and devalue their own currencies.)

So, bottom line is this:

“Short bond positions” will see volatility depending on what’s happening with the ECB balance sheet, because it will directly affect Treasuries. But, the trend should remain lower in bonds as long as the ECB remains committed to balance sheet expansion. So, don’t get spooked by counter-trend rallies.

For “long Europe” equity positions, the trend upward should be more smooth, as stocks are clearly viewing “bad as good” in Europe—as long as the expectation remains that the ECB will eventually do QE. Point being, the trends (Treasuries down, European stocks up) remains in place despite the fact we’re likely to see some short term counter trend moves.

To learn more, sign up for a two week free trial on the right hand side of this page.