Term Structure in Natural Gas Has Turned Bullish

Any real commodity trader or analyst knows that watching the “term structure” of commodities can offer substantial insight into whether the trend in that commodity is turning bullish, or bearish.

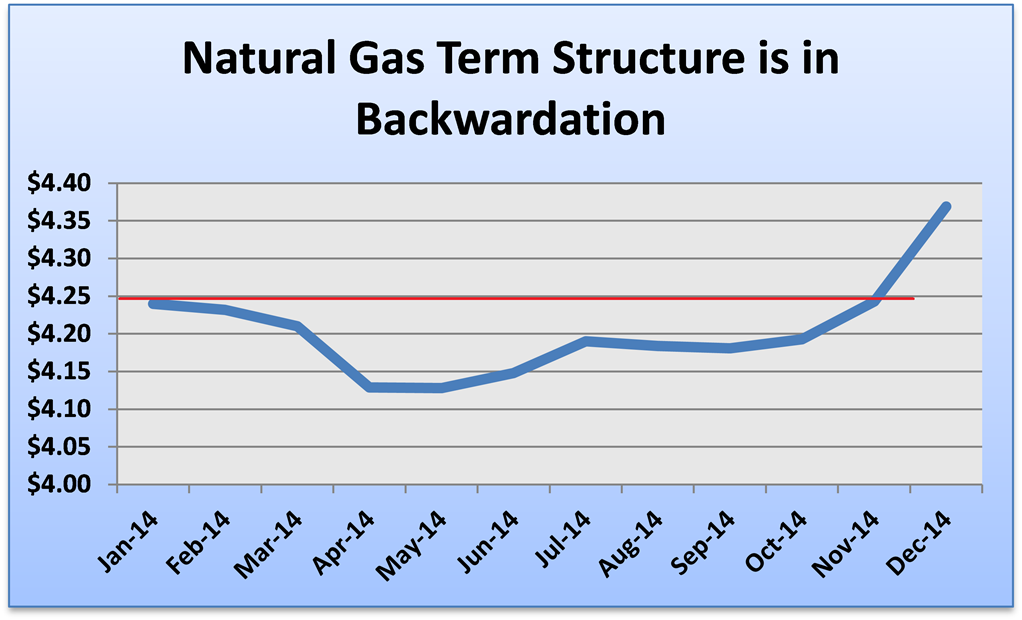

The term structure of natural gas has become significantly “backward-dated” in that the current month’s prices (for January delivery) are trading higher than February’s price. Prices for February delivery are trading at a higher price than March delivery, and this lasts all the way out until June 2014. Term structures can be an important indicator of physical demand for a commodity, and as the backwardation in natural gas implies, we are seeing a systemic increase in demand for natural gas—not just a temporary uptick in demand due to cold weather to start the winter. And, that is potentially bullish not just for natural gas, but for natural gas producers.

Last week I mentioned that the natural gas “E&Ps” (short for exploration and production companies) have badly lagged this spike in natural gas, and oftentimes that happens as the market assumes the spike in natural gas is temporary.

But, if the term structure in natural gas is telling us a more bullish story, then the case can be made that natural gas E&Ps offer potential value in the market over the medium and longer term.

The best “pure play” E&P ETF is the First Trust ISE Revere Natural Gas Index Fund (FCG), which I mentioned last Tuesday. That ETF got hit late last week thanks to a drop in Penn Virginia Corp. (PVA), the second-largest holding. But, medium/longer term, it does offer the best “pure play” exposure to natural gas E&Ps. A secondary, and more liquid option, is the SPDR S&P Oil & Gas Exploration & Production ETF (XOP). But, XOP isn’t as much of a “pure play” on natural gas E&Ps, as they only make up 75% of the fund. Refiners (15%) and integrated oils (5%) represent the other sub-industries in this ETF.

Finally, I’m not a single-stock guy so everyone needs to do their own research, but I did ask some colleagues for their favorite names in the natural gas E&P space, so here are some of them: COG, AR, EOG, NFX, ATLS, ARP. Again, I haven’t “explored” these single stocks, but I wanted to provide some individual names for people to look at, if interested.

Bottom line is, longer term the future for natural gas is attractive, even in the face of surging supply, because natural gas is one of the few commodities where the market is inventing new sources of demand (gas-fired power plants, natural-gas-powered cars, exports of LNG, etc.). And, although in the short term natural gas itself is stretched and I wouldn’t buy the commodity at these levels, the equities may offer value if the term structure is forecasting a structural rise in demand.

If you’ve found this analysis useful, I invite you to try a free trial of The 7:00′s Report (pronounced The Seven’s Report) by clicking here.

Subscribers to The 7:00′s Report include financial advisors from major bulge bracket firms, RIA’s, multi-billion dollar asset management companies, hedge funds, as well as sophisticated investors. Again, if you’d like sign up for a free trial, please click here.