Gold futures declined yesterday, initially thanks to a stronger dollar; however, a reversal in the greenback saw precious metals close well off the worst levels of the day. Gold futures declined 0.34% on the day.

It is clear that the precious metals market, specifically gold, has gotten crushed since the election, and there are a lot of investors wondering if now is the time to buy.

The simple answer is, “Not yet.”

Longer term, given The Sevens Report is positive on inflation, gold will rally again, but The Sevens Report needs to see higher inflation to offset two strong headwinds on gold near term.

First, a lot of this reversal was thanks to the unexpected election outcome that initiated the rally in the dollar to multi-year highs. When the dollar rallies hard, gold will fall every time. Going forward, the dollar rally will need to level off in order for the gold market to materially stabilize. The Sevens Report long-term upside target for the Dollar Index is between 106 and 107, so until The Sevens Report see those levels (or signs of a significant reversal in the greenback confirmed by some sort of fundamental altering event) the outlook for gold is not very bright… until The Sevens Report sees an acceleration in inflation.

Aside from the dollar, the real interest rate (nominal interest rates minus the inflation rate) has offered the best fundamental read for the gold market.

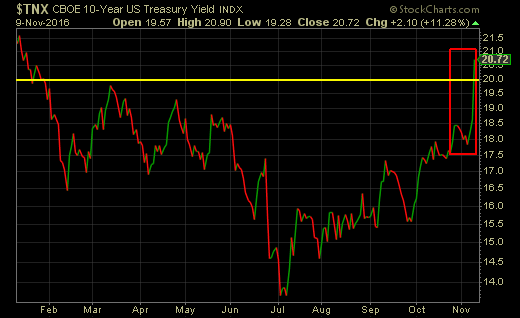

In the wake of the election, inflation expectations did not materially change; however, nominal interest rates surged in a big way. That resulted in a spike in real interest rates, and that’s very bearish for gold.

When inflation accelerates, and starts to outpace rising interest rates again, The Sevens Report will see gold as an attractive investment like it did earlier this year.

Remember, Treasuries were trading sideways this summer and inflation was firming, which led to declining real interest rates (which is bullish gold). But if the trend in interest rates is materially higher and inflation remains well contained, gold will likely fall further.

To be clear, gold and the dollar can rally together, just not while the dollar is moving as swiftly as it did post-election. If inflation shows signs of getting out of hand, and the Fed is perceived to be “behind the curve,” then gold can rally (because real interest rates will decline as inflation accelerates despite a rally in the buck).

Technically speaking, the trend is lower in gold, and there is not much support before the $1130-$1140 area. To the upside, retracements to resistance at either $1210 or $1225 should be normal throwbacks in an otherwise downward trending market.

Bottom line, gold is not a buy now. But as market conditions settle, The Sevens Report will look for the two key components necessary for a new rally in gold… the dollar leveling off and real inflation rates showing signs of declining as actual inflation edges higher.