Economic Indicators: U.K. GDP Drop and EU Industrial Production

Economic Indicators: Tom Essaye Quoted in Barron’s

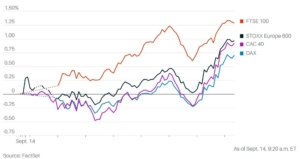

Gloomy Economic Data Weigh on European Trading

Economic indicators such as, “U.K. GDP dropped…after hot wage data yesterday, bolstering stagflation fears while EU Industrial Production fell,” said Tom Essaye, the founder of Sevens Report Research.

“Despite the recently soft data, rates markets continue to price in a 75% chance of an ECB rate hike this week.”

Also, click here to view the full Barron’s article published on September 13th, 2023. However, to see Tom’s full comments on the current market environment sign up here.

If you want research that comes with no long term commitment, yet provides independent, value added, plain English analysis of complex macro topics, then begin your Sevens Report subscription today by clicking here.

To strengthen your market knowledge take a free trial of The Sevens Report.

Join hundreds of advisors from huge brokerage firms like Morgan Stanley, Merrill Lynch, Wells Fargo Advisors, Raymond James, and more! To start your quarterly subscription and see how The Sevens Report can help you grow your business, click here.